How to Reply to GST Summons from DGGI – Step-by-Step Guide

Receiving a formal notice from a government authority like the Directorate General of GST Intelligence (DGGI) can be stressful for any business owner or individual. This legal document, known as a summons, carries significant weight and demands immediate, careful attention. Understanding how to correctly reply to DGGI summons is not just about compliance; it’s about protecting your rights and ensuring the process is handled smoothly. This comprehensive guide will provide a clear, step-by-step process on how to respond correctly, detailing the entire DGGI summons response procedure and offering essential legal guidance for summons in India to help you navigate this challenging situation with confidence.

What is a DGGI Summons and Why Did You Receive One?

Fear often stems from the unknown. By understanding what a DGGI summons is and why it might have been issued to you, you can approach the situation with clarity and composure. A summons is not an accusation of guilt; it is a formal request for information or evidence as part of an ongoing inquiry.

Decoding the DGGI (Directorate General of GST Intelligence)

The DGGI is the apex intelligence and investigation agency for matters related to the Goods and Services Tax (GST). Functioning under the Central Board of Indirect Taxes and Customs (CBIC), its primary mandate is to detect and prevent tax evasion across the country. DGGI officers are empowered to conduct inquiries, audits, searches, and seizures to unearth fraudulent activities, such as the use of fake invoices for claiming Input Tax Credit (ITC), undervaluation of goods, or non-payment of GST. To understand this process better, read our detailed guide on GST Investigation by DGGI – What It Means & Why You Are Selected. Think of them as the specialized investigation wing that handles complex and large-scale GST fraud cases.

Understanding the Legal Basis: Section 70 of the CGST Act, 2017

The power to issue a summons comes from a specific law. A DGGI summons is issued under the authority of Section 70 of the Central Goods and Services Tax (CGST) Act, 2017. This section grants a duly authorized GST officer the power to summon any person whose attendance they consider necessary. For a deeper understanding of the legal framework, it is helpful to know the Powers of GST Officers During Investigation (Section 67, 70, 74 Explained). The purpose can be twofold: either to give evidence (testimony) under oath or to produce specific documents or any other relevant articles for an ongoing investigation. The proceedings under a summons are deemed to be “judicial proceedings,” which means any statement you provide holds legal weight and can be used as evidence. This is a critical aspect of the summons reply process India and underscores the need for a truthful and cautious approach.

Common Triggers for a DGGI Summons

You might be wondering what specific activity could have prompted this notice. While every case is unique, summons are generally issued when the department’s data analytics or intelligence gathering points towards potential discrepancies. A clear understanding DGGI summons response begins with knowing the likely cause.

- Significant Data Mismatches: A major red flag for tax authorities is a substantial difference between the data in your GSTR-1 (outward supplies), GSTR-3B (summary return), and the auto-populated GSTR-2A/2B (purchase-related data).

- Suspected Availment of Fake Input Tax Credit (ITC): The DGGI actively investigates networks that create fake invoices without the actual supply of goods or services. If your business has transactions with a supplier who is under investigation, you may be summoned to provide evidence.

- Discrepancies in E-way Bills: The department cross-verifies E-way bill data with GST returns. Any significant mismatch between the goods declared in E-way bills and the turnover reported in returns can trigger an inquiry.

- Intelligence from Other Agencies or Whistleblowers: The DGGI often acts on specific intelligence received from other government bodies (like the Income Tax Department) or from whistleblowers about potential tax evasion.

- Unusually High Refund Claims: Claiming large GST refunds, especially for inverted duty structures or exports, can lead to detailed scrutiny if the claims appear disproportionate to the nature of your business.

First Steps After Receiving a Summons: Don’t Panic, Prepare!

The moment you receive a summons, your immediate actions are crucial. Panic can lead to mistakes, while a methodical approach ensures you stay in control. Follow these initial steps to lay the groundwork for a compliant and effective response.

Step 1: Verify the Authenticity of the Summons

Before you take any other action, you must confirm that the summons is genuine. Every official communication from the CBIC, including a summons, must have a computer-generated Document Identification Number (DIN). You can and should verify this DIN on the official government portal. Look for the issuing officer’s name, designation, and the official stamp or seal. An authentic summons will clearly state the legal provision (Section 70 of the CGST Act) under which it has been issued.

Actionable Tip: Verify the DIN on the CBIC’s DIN Verification Portal. This simple check can protect you from potential scams.

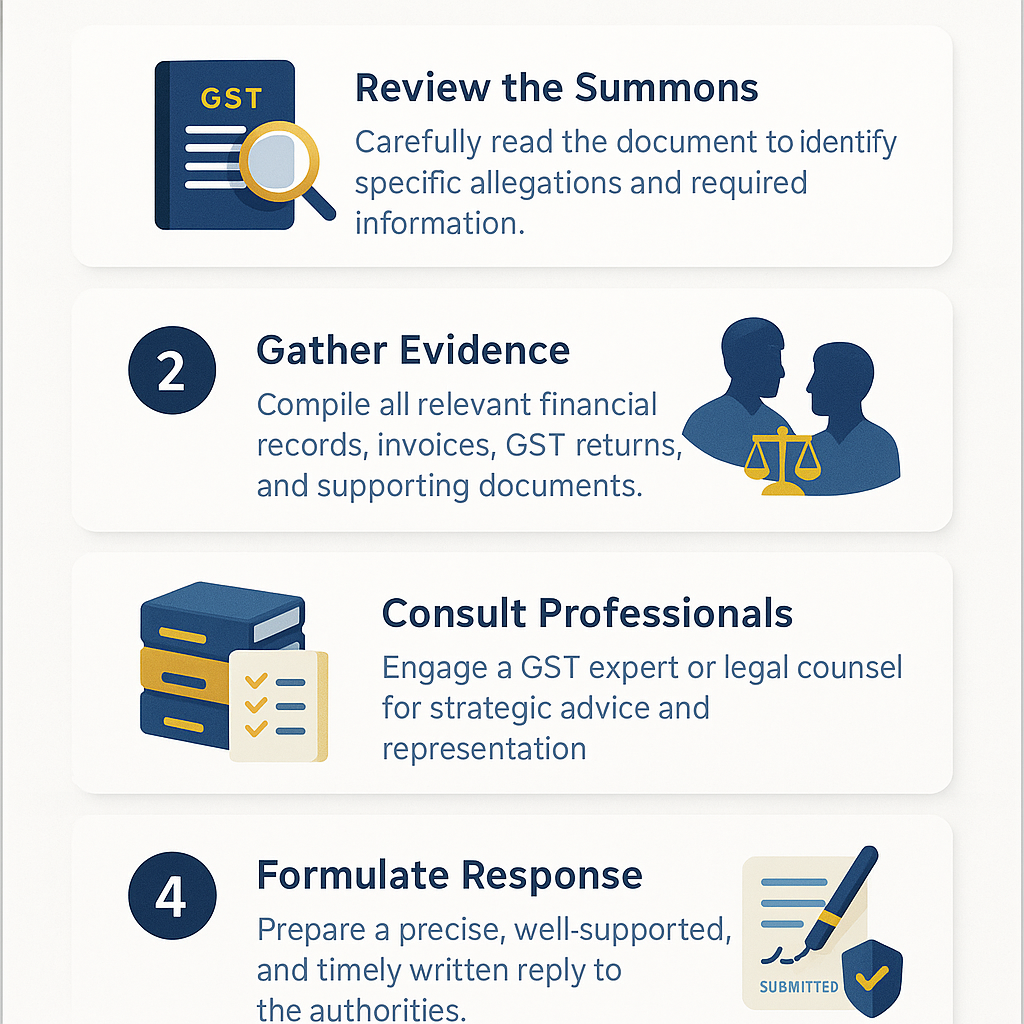

Step 2: Read the Summons Carefully

Once authenticated, read the document multiple times to fully comprehend its requirements. Pay close attention to the details. Are you being summoned for a personal appearance to give a statement? Or are you required to submit specific documents? Often, it is a combination of both. Note the exact date, time, and address where you are required to be present. The summons will also list the documents you need to produce, such as sales invoices, purchase ledgers, bank statements, or GSTR filings for a specific period. Misinterpreting these instructions can lead to an incomplete or incorrect response.

Step 3: Do Not Ignore the Summons

This cannot be stressed enough: never ignore a DGGI summons. It is a legal directive, and non-compliance has serious consequences. Ignoring it is an offense under both the CGST Act and the Indian Penal Code (IPC). The authorities can issue penalties and even initiate prosecution for non-cooperation. Acknowledging the summons and preparing to comply is the only correct course of action. This piece of legal guidance for summons in India is fundamental to avoiding further complications.

Step 4: Seek Professional Legal Guidance Immediately

While you might be tempted to handle the matter yourself, it is highly advisable to seek professional help. A summons is the beginning of a formal legal proceeding. Consulting an experienced tax professional, such as a Chartered Accountant or a Tax Lawyer, is a critical step. An expert can help you interpret the legal language of the summons, understand the potential implications, assist in gathering and organizing the required documents, and prepare you for the statement recording. This guidance is invaluable for navigating the complex DGGI summons response procedure and protecting your legal interests.

Call to Action: The experts at TaxRobo specialize in handling such tax notices. Contact us for professional guidance on your summons response.

A Step-by-Step Guide for a Compliant Reply to DGGI Summons

Once you have completed the initial steps, it’s time to prepare your formal response. This involves a meticulous process of document collection, personal preparation, and understanding your rights and responsibilities during the inquiry. A proper reply to DGGI summons requires careful execution of each of these stages.

Part A: Gathering and Organizing Documents

The summons will specify the documents required by the investigating officer. Your first task is to collate these meticulously. Create a master file with all the original documents and make at least two sets of clear photocopies—one for submission and one for your own records.

Here is a common checklist of documents that may be requested:

- GST Registration Certificate: A copy of your business’s GST registration.

- GST Returns: All relevant returns for the period under investigation, including GSTR-1, GSTR-3B, and GSTR-9/9C.

- Sales and Purchase Invoices: The specific tax invoices related to the transactions being scrutinized.

- Bank Statements: All business bank account statements for the relevant period.

- Ledgers and Registers: Copies of your sales ledger, purchase ledger, and stock registers.

- E-way Bills: E-way bills generated for the movement of goods in question.

- Other Supporting Documents: Any contracts, agreements, or other documents specifically requested in the summons.

Pro-Tip: Organize the documents chronologically and label them clearly. This demonstrates professionalism and cooperation, making the process smoother for both you and the officer.

Part B: Preparing for the Personal Appearance

If the summons requires your personal attendance, preparation is key. How you conduct yourself can significantly impact the proceedings. Here are some essential DGGI summons response tips to keep in mind.

| Do’s | Don’ts |

|---|---|

| Be Punctual: Arrive at the designated location at least 15 minutes before the scheduled time. | Do Not Argue: Avoid getting into arguments or debates with the investigating officer. Maintain a respectful demeanor. |

| Carry Identification: Always carry a valid government-issued photo ID like an Aadhaar Card or PAN Card. | Do Not Provide False Information: Lying under oath is a serious offense (perjury). Stick to the facts. |

| Bring All Documents: Carry the original documents and the prepared photocopy sets with you. | Do Not Sign Blank Papers: Never sign any blank or pre-written statement. |

| Be Cooperative: Answer all questions politely and truthfully. Cooperation is viewed favorably. | Do Not Be Vague: Provide clear, concise answers. If you don’t know an answer, say so instead of guessing. |

| Stay Calm: Maintain your composure. If you feel stressed, take a moment to breathe and think before you speak. | Do Not Volunteer Unsolicited Information: Answer only the questions that are asked. |

Part C: During the Statement Recording

The statement recording is a formal process. An officer will ask you questions about your business operations and the documents you have submitted. This statement is recorded in writing under oath and holds significant legal value. You have certain rights during this process. You have the right to read the entire statement carefully after it has been recorded. If you find any inaccuracies or if something has been misquoted, you must insist on correcting it before you sign. Do not sign a statement that you do not fully agree with. You also have the right to request a copy of your recorded statement for your records, which is crucial for any future proceedings. This part of the summons reply process India is where professional guidance is most valuable.

What Happens After You Reply to DGGI Summons?

Submitting documents and recording a statement is a major step, but it is not necessarily the end of the inquiry. Understanding the potential outcomes will help you manage expectations and prepare for what lies ahead after you reply to DGGI summons.

Possible Outcomes

Based on your submissions and statement, the investigation can proceed in one of several directions.

- Case Closure: If the officer is satisfied with the documents, explanations, and evidence provided, and finds no discrepancies, the inquiry may be concluded and the case closed. This is the best-case scenario.

- Further Investigation: The officer might find that more information is needed to complete the inquiry. In this case, they may issue another summons for additional documents or call you for further questioning to clarify certain points.

- Issuance of a Show Cause Notice (SCN): If the investigation reveals evidence of tax evasion, short payment of tax, or wrongful availment of ITC, the department will issue a formal Show Cause Notice. The SCN is a detailed document that outlines the department’s findings and proposes a demand for the unpaid tax, along with applicable interest and penalties. You will be given an opportunity to reply to the SCN before a final order is passed. This step is critical, and you can learn more by reading How to Respond to a GST Show Cause Notice: A Step-by-Step Guide.

The Importance of Follow-up and Record-Keeping

Regardless of the outcome, it is vital to maintain a complete and organized file of the entire process. This file should contain a copy of the summons, proof of submission of documents, a copy of your recorded statement, and any other correspondence with the department. All follow-up communication should be done formally and preferably through your tax consultant to ensure there is a proper record of all interactions. This documentation is your defense and record for any future legal proceedings.

Conclusion

Receiving a notice from the DGGI can be daunting, but it is a manageable legal process. A DGGI summons must always be taken with the utmost seriousness, and the correct approach is to remain calm, verify its authenticity, immediately seek professional help, and cooperate truthfully with the authorities. A timely and well-prepared reply to DGGI summons is your best strategy to protect your interests, demonstrate compliance, and avoid the severe legal and financial penalties that can result from non-cooperation. By following this guide, you can navigate the inquiry with confidence and work towards a fair resolution.

Final CTA: Navigating the complexities of a GST investigation requires expertise. Don’t leave it to chance. Contact the TaxRobo team today for end-to-end assistance with your DGGI summons response procedure.

Frequently Asked Questions (FAQs) about DGGI Summons

Question 1: Can I ask for more time to appear or submit documents?

Answer: Yes. If you have a genuine reason (such as a medical emergency or the need for more time to collate extensive documents), you can file a formal written request for an adjournment. Clearly state the reason for the request and propose an alternative date. The decision to grant an extension is entirely at the discretion of the issuing officer.

Question 2: What are the penalties for not complying with a DGGI summons?

Answer: Failure to comply with a summons without a valid reason can attract a penalty of up to ₹25,000 under Section 122 of the CGST Act. Additionally, it can lead to prosecution under Section 174 (non-attendance in obedience to an order from a public servant) and Section 175 (omission to produce a document) of the Indian Penal Code.

Question 3: Can my CA or lawyer appear on my behalf?

Answer: A summons under Section 70 is typically issued to a specific person (like a director, partner, or proprietor) whose evidence is considered necessary for the inquiry. Therefore, you are generally required to appear in person. While your authorized representative (CA or lawyer) can help you prepare documents and may be allowed to accompany you, they cannot give a statement on your behalf unless the officer specifically permits it.

Question 4: Is the statement given to a GST officer admissible in court?

Answer: Yes, absolutely. A statement recorded under oath during a summons proceeding under Section 70 of the CGST Act is considered a part of a “judicial proceeding.” This means it is fully admissible as evidence against you in a court of law. This is a critical point that highlights the need for truthful answers and sound legal guidance for summons in India.