GST Summons to Director or Partner – A Complete Guide on How to Respond

Receiving a formal notice from a tax authority can be a daunting experience for any business leader. The key is not to panic but to respond correctly and professionally. This blog post is a comprehensive guide on understanding and handling a GST summons to director or partner. We will break down what a summons is, why you might receive one, and the precise steps you need to take. A GST summons is a legal proceeding, and an improper response can lead to significant penalties, making it crucial to understand the correct protocol for compliance and to protect your business interests. This guide will provide actionable steps for responding to GST summons India effectively, ensuring you navigate the process with confidence and clarity.

What Exactly is a GST Summons and Why Was It Sent to You?

To properly address a summons, you must first understand its legal standing and the common triggers that lead to its issuance. A summons is not merely a request for information; it is a legally binding call for your presence and cooperation in an official inquiry. Demystifying this notice is the first step toward a compliant and stress-free response.

Understanding the Legal Framework: Section 70 of the CGST Act

A GST summons is a legal document issued under the authority of Section 70 of the Central Goods and Services Tax (CGST) Act, 2017. This section grants authorized GST officers the power to summon any person whose attendance they consider necessary for an inquiry. The purpose is twofold: either to compel an individual to provide evidence (“give evidence”) or to produce specific documents and other materials (“produce a document or any other thing”) relevant to the investigation. Understanding the full scope of these is covered in our guide on the Powers of GST Officers During Investigation (Section 67, 70, 74 Explained).

It’s vital to recognize the gravity of this notice. The law specifies that any inquiry conducted under a summons is treated as a “judicial proceeding” within the meaning of Section 193 and Section 228 of the Indian Penal Code. This means that providing false information can lead to prosecution for perjury, and any act of intentional insult or interruption to the officer can be treated as a criminal offense. You can read the full text of the law on the official CBIC website.

External Resource: Central Goods and Services Tax (CGST) Act, 2017

Common Reasons a Director or Partner Receives a GST Summons

A summons is typically issued when the GST department is investigating a specific issue and requires your direct input or documentary evidence. While the reasons can vary, they usually stem from data discrepancies or suspected non-compliance. Understanding these triggers can help you anticipate the focus of the inquiry.

Here are some common reasons why a GST summons for partners in India or directors is issued:

- Significant Mismatches in GST Returns: One of the most frequent triggers is a discrepancy between the data reported in GSTR-1 (outward supplies) and GSTR-3B (summary return with tax payment). Similarly, mismatches between GSTR-3B and GSTR-2A/2B (auto-populated input tax credit) can raise red flags.

- Investigation into Suspected Tax Evasion: If the department has intelligence suggesting that your company is under-reporting its sales, inflating expenses, or evading tax in any other manner, a summons may be issued to the key managerial personnel.

- Fraudulent Input Tax Credit (ITC) Claims: The authorities are particularly vigilant about fraudulent ITC. If your company has claimed ITC from a supplier who is found to be non-existent, has issued fake invoices, or has not paid their taxes, you may be summoned to provide clarification and documentation for your claims. Navigating such allegations requires understanding the potential legal ramifications, which are detailed in our guide on Fake ITC Cases in GST – Penalty, Arrest & Defence Strategy.

- Third-Party Inquiry: Your business might not be the primary target of the investigation. You could receive a summons if one of your major suppliers or customers is under scrutiny. In such cases, the department needs you to act as a witness or provide transactional documents to corroborate or refute claims related to that third party.

- Prolonged Non-Compliance: Consistently failing to file GST returns or respond to basic notices can escalate the matter, leading the department to issue a summons to ensure compliance. Mastering the basics is key, and our guide on How to File GST Returns Online: A Step-by-Step Guide of the GST Filing Process & Procedure can prevent such issues. This is a common issue when it comes to responding to GST notices for companies.

- Involvement with Fake Invoicing or Shell Companies: If your company’s GSTIN is linked in any way to transactions with known shell companies or entities involved in circular trading or fake invoicing rackets, the directors or partners will be summoned to explain their involvement.

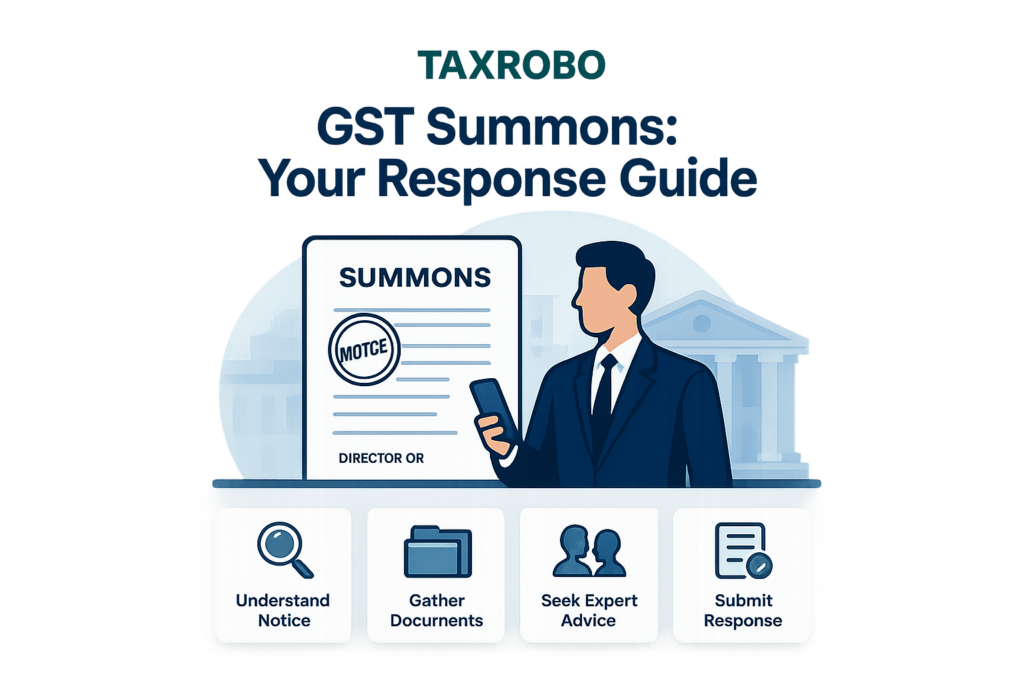

The Ultimate Step-by-Step GST Summons Response Guide for Directors

Receiving a GST summons to director or partner requires a methodical and calm response. Panicking or ignoring the notice will only worsen the situation. The following step-by-step guide provides a clear, actionable checklist that you can follow to ensure you handle the process correctly and protect your interests.

Step 1: Immediate Actions – Don’t Panic, Don’t Ignore

The most critical first step is to treat the summons with the seriousness it deserves. Ignoring it is a punishable offense under the law. Upon receiving the document, take a deep breath and immediately perform the following actions:

- Read the Entire Document Carefully: Go through every line of the summons. Pay close attention to the name of the issuing officer, their designation, and the office address.

- Note Key Details: Immediately mark your calendar with the date, time, and location where you are required to appear.

- Identify Requested Information: The summons will specify the documents or information you need to produce. Make a clear checklist of these requirements. It might ask for financial statements, invoices, bank statements, ledgers, or contracts related to a specific period or transaction.

Step 2: Verify the Authenticity of the Summons

In today’s digital age, it is crucial to protect yourself from fraudulent notices. Every genuine notice or summons issued by the CBIC must have a computer-generated Document Identification Number (DIN). Verifying this DIN is a non-negotiable step to confirm the authenticity of the communication.

Here’s how to do it:

1. Locate the DIN on the summons document. It is usually mentioned in the header or footer.

2. Visit the official CBIC DIN verification portal.

3. Enter the DIN exactly as it appears on the notice and complete the captcha.

4. The portal will display the details of the notice if it is genuine. If the DIN is not found, you should immediately contact the concerned GST office to report the potentially fake notice.

Official Portal: CBIC DIN Verification Search

Step 3: Seek Professional Legal or Tax Advice Immediately

Once you have verified the summons, your next call should be to a qualified professional. Do not attempt to handle this complex legal matter on your own. A seasoned tax consultant or a lawyer specializing in GST litigation will be your most valuable asset.

Here is how an expert can help:

- Interpret the Summons: They can decipher the legal language and help you understand the precise nature of the inquiry and what the authorities are investigating.

- Strategize the Response: An expert will guide you on preparing a legally sound response and help you collate the exact documents required, ensuring you don’t inadvertently provide incriminating or irrelevant information.

- Advise on Your Rights and Obligations: They will brief you on your legal rights during the hearing—such as the right to a copy of your statement—and your obligations to cooperate truthfully. This is a key part of our GST summons response guide for directors.

Internal CTA: TaxRobo’s team of experts specializes in GST compliance and litigation. We can help you navigate the complexities of responding to GST summons in India. Contact us for an online CA consultation today.

Step 4: Prepare and Organize All Required Documents

The summons will explicitly list the documents you need to bring. Meticulous preparation is key to a smooth proceeding.

- Create a Master File: Systematically gather all the documents mentioned, such as copies of GST returns, specific sales or purchase invoices, bank statements for the relevant period, ledgers, e-way bills, and any contracts or agreements.

- Organize and Index: Arrange the documents logically, perhaps chronologically or by transaction type. Create an index page so you can quickly locate any document the officer asks for.

- Make Photocopies: Never submit original documents without getting a formal, signed acknowledgement from the officer. It is a best practice to prepare two sets of photocopies: one for submission and one for your own records. Bring the originals with you for verification, but hand over only the copies unless specifically instructed otherwise.

Step 5: Preparing for the Personal Appearance

Your personal appearance is where your statement will be recorded under oath. Your preparation and demeanor during this session are critical. This is where you can learn how directors should respond to GST summons in person.

Here are some essential tips:

- Be Truthful and Factual: Your statement is admissible evidence in court. Stick strictly to the facts. If you do not know the answer to a question, it is better to say so than to speculate or provide incorrect information.

- Remain Calm and Concise: Answer the questions asked calmly and to the point. Avoid volunteering excess information that is not directly relevant to the question.

- Know Your Rights: You have the right to request that your statement be recorded in a language you are most comfortable with. You can also request a break if you feel tired or overwhelmed.

- Role of Legal Counsel: While your lawyer cannot be present with you during the actual recording of the statement, they are permitted to wait outside the room. You can consult with them before the session begins and after it concludes.

The Do’s and Don’ts When Facing a GST Summons

To simplify, here is a quick summary of best practices in a scannable format.

The Do’s

- ✅ Do attend the summons on the specified date and time. If you are genuinely unable to attend, you must submit a formal written request for an adjournment to the issuing officer well in advance, stating a valid reason.

- ✅ Do carry a government-issued photo ID like your Aadhar Card or PAN Card for personal verification.

- ✅ Do cooperate fully with the GST officials during the inquiry. A cooperative attitude can make the process smoother.

- ✅ Do request a copy of your recorded statement after the proceeding is complete. You are legally entitled to it.

The Don’ts

- ❌ Don’t provide any false, fabricated, or misleading information. As this is a judicial proceeding, doing so can lead to prosecution for perjury under the Indian Penal Code.

- ❌ Don’t argue, lose your temper, or be disrespectful towards the tax officials. Maintain a professional and calm demeanor throughout.

- ❌ Don’t sign any statement or document without reading it thoroughly and understanding its contents completely.

- ❌ Don’t submit original documents unless it is absolutely unavoidable, and only after receiving a detailed, signed acknowledgement from the officer.

Conclusion

Receiving a GST summons to director or partner is undoubtedly a serious legal matter that demands a structured, careful, and prompt response. It is not something to be feared but to be managed professionally. The key takeaways are to act immediately, verify the notice’s authenticity, seek expert guidance from a tax professional, prepare all documentation diligently, and respond truthfully and calmly during the appearance. While the process can be stressful, remember that a well-prepared, transparent, and compliant approach is the best strategy to ensure a smooth resolution and safeguard the interests of your business.

Don’t navigate GST complexities alone. If you need help with a GST summons or any other tax notice, TaxRobo’s expert team is here to provide a clear path forward. Contact us for a consultation today.

Frequently Asked Questions (FAQs)

Q1: What are the consequences of not complying with a GST summons?

A: Non-compliance is a serious offense. It can lead to a penalty of up to ₹25,000 under Section 122 of the CGST Act. Additionally, the GST officer can initiate proceedings against you under Section 174 of the Indian Penal Code (IPC) for non-attendance in obedience to an order from a public servant, which can involve further legal action.

Q2: Can I authorize my accountant or employee to attend the summons on my behalf?

A: No. A summons under Section 70 is issued to a specific person, i.e., the director or partner named in the notice. The personal appearance of the individual summoned is mandatory. While an authorized representative or a lawyer may accompany you to the GST office, they cannot appear or give a statement on your behalf.

Q3: Is the statement I give to the GST officer admissible in court?

A: Yes, absolutely. A proceeding under a GST summons is deemed to be a “judicial proceeding.” Therefore, any statement recorded by the officer is given under oath and is fully admissible as evidence in a court of law or before other legal authorities. This is precisely why it is critical to be truthful, accurate, and careful with your words.

Q4: How much time is generally given to appear for a summons?

A: The law does not specify a fixed timeframe. The time provided is at the discretion of the issuing officer but is generally a reasonable period (often 7-15 days) to allow the summoned person to prepare and gather the necessary documents. If you require more time due to a genuine reason (e.g., travel, illness, or the need to collect extensive data), you must submit a written request for an adjournment to the officer who issued the summons.