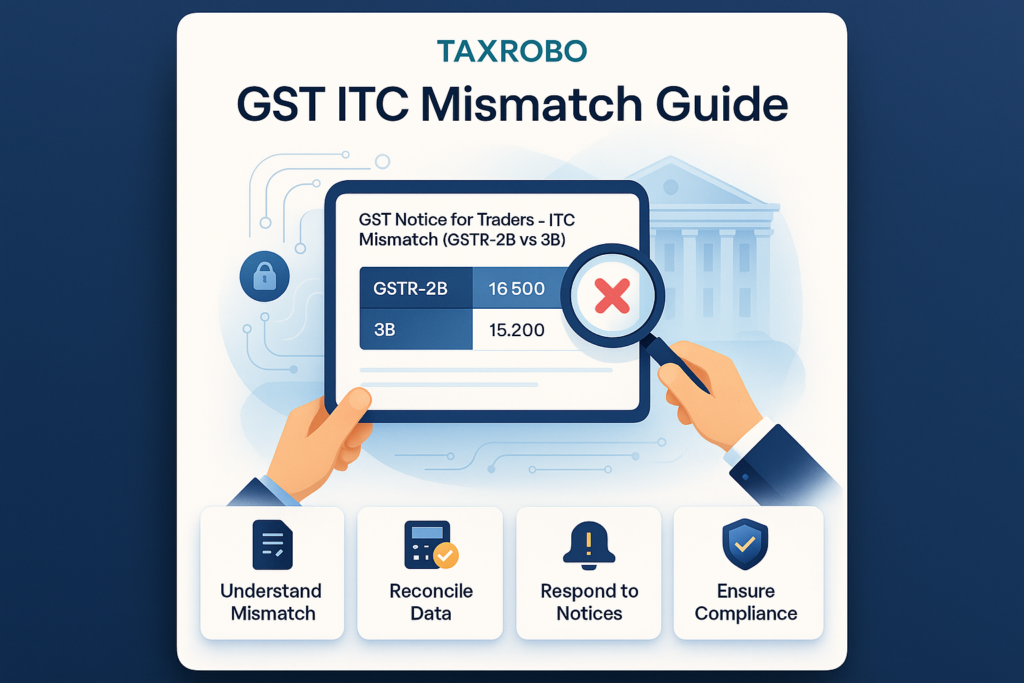

GST Notice for Traders – ITC Mismatch (GSTR-2B vs 3B) Complete Guide

Received a scary-looking GST notice about an ITC mismatch? Before you panic, know that you’re not alone. This is a common issue faced by many Indian traders, and understanding how to navigate it is crucial for your business’s health. This complete ITC mismatch guide is designed specifically to demystify the process for you. An Input Tax Credit (ITC) mismatch between your GSTR-2B and GSTR-3B is a primary reason for scrutiny from the GST department, and ignoring it can lead to hefty penalties and serious business disruptions. This article will break down the problem, provide a clear GSTR-2B vs 3B explanation, and give you actionable steps to handle any GST notice for traders India with confidence.

Understanding the Basics: What is an ITC Mismatch?

To effectively tackle a mismatch notice, it’s essential to first grasp the fundamental concepts involved. The terms ITC, GSTR-2B, and GSTR-3B are at the heart of your GST compliance journey. Understanding their individual roles and how they interact is the first step toward preventing and resolving discrepancies. Think of this as learning the rules of the game before you start playing; it equips you to make informed decisions and avoid common pitfalls that many businesses encounter.

First, What is Input Tax Credit (ITC)?

In simple terms, Input Tax Credit (ITC) is the credit a business can claim on the GST it paid for its purchases and expenses (inputs). This claimed credit is then used to reduce the amount of GST it needs to pay on its sales (outputs). Think of it as a discount on your final tax bill, making it a crucial component for your business’s cash flow and profitability. For traders, who deal with a high volume of purchases, managing ITC correctly is not just a compliance requirement but a significant financial tool. When you purchase goods for your shop for ₹100 and pay ₹18 as GST, that ₹18 becomes your ITC, which you can use to offset the tax you collect from your customers.

The Core of the Issue: GSTR-2B vs 3B Explanation

The entire mismatch issue boils down to the difference between two key GST returns. While they might seem similar, they serve very different purposes, and their comparison is what the GST system uses to flag potential discrepancies. Properly understanding GST returns for traders is vital. Here’s a clear breakdown:

| Feature | GSTR-2B (Your Eligibility Report) | GSTR-3B (Your Declaration) |

|---|---|---|

| Nature | Auto-generated, static, read-only statement. | A summary return you manually prepare and file. |

| Source of Data | Data is pulled from your suppliers’ GSTR-1/IFF filings. | Data is entered by you based on your own books of accounts. |

| Purpose | Shows the eligible ITC available to you for a specific month. | Declares your total sales, tax liability, and the ITC you are actually claiming. |

| Analogy | It’s the “Report Card” the government sees for your eligible ITC. | It’s your “Declaration Form” where you state the ITC you are taking. |

A mismatch occurs when the ITC you claim in your GSTR-3B is higher than the eligible ITC shown in your auto-populated GSTR-2B. The GST portal’s automated systems are designed to catch this difference, which then triggers an electronic notice.

Why Do ITC Mismatches Happen? Common Causes for Traders

An ITC mismatch is rarely a deliberate act of non-compliance; more often, it stems from clerical errors, timing differences, or miscommunication between you and your suppliers. Identifying the root cause is the most critical step in resolving GSTR-2B discrepancies. These issues can typically be categorized into two groups: errors originating from your supplier’s side and mistakes made on your own end during filing.

Errors from Your Supplier’s End

Often, the reason for the mismatch lies not with you, but with the actions (or inactions) of the businesses you buy from. Since your GSTR-2B is entirely dependent on what your suppliers report, any error they make directly impacts your available credit.

- Late Filing: This is the most common reason. Your supplier may have filed their GSTR-1 (sales return) after the due date for the month. As a result, the invoice they issued to you did not appear in your GSTR-2B for that specific month and will only appear later, causing a temporary mismatch.

- Incorrect Details: A simple typo can cause major issues. The supplier might have entered the wrong GSTIN for your business, an incorrect invoice number, the wrong date, or an inaccurate tax amount in their GSTR-1.

- B2C Instead of B2B: In a hurry, your supplier might mistakenly report your Business-to-Business (B2B) purchase as a Business-to-Consumer (B2C) sale. B2C sales don’t get reflected in any GSTR-2B, meaning you won’t see the eligible credit.

- Quarterly vs. Monthly Filing: If your supplier is registered under the QRMP (Quarterly Return Monthly Payment) scheme, they file their detailed GSTR-1 only once a quarter. If you file your GSTR-3B monthly, there will be a natural mismatch for the first two months of that quarter until they file their quarterly return.

Errors from Your End

It’s also important to review your own processes, as mistakes can happen during data entry or interpretation of GST rules. These self-inflicted errors are entirely within your control to prevent and rectify.

- Typographical Errors: You might have made a data entry mistake while filling out the ITC figures in your GSTR-3B, accidentally claiming a higher amount than what’s on the actual purchase invoice.

- Claiming Ineligible Credit: You may have inadvertently claimed ITC on goods or services that are “blocked” under Section 17(5) of the CGST Act. For a detailed list, see our guide on Blocked Credits Under Section 17(5): What ITC Cannot Be Claimed?. Common examples for traders include GST paid on commercial vehicles with less than 13-person capacity, or expenses on food and beverages.

- Timing Mismatch: You received an invoice and the goods in January but claimed the ITC in January’s GSTR-3B. However, your supplier filed their return late, so the invoice appeared in February’s GSTR-2B. This creates a mismatch for January.

- Duplicate Claims: A simple oversight could lead to you claiming ITC for the same purchase invoice in two different months, artificially inflating your total credit.

The GST Notice: Understanding Form DRC-01C

When the GST Network’s automated system detects a significant difference between the ITC you claimed in GSTR-3B and the amount available in your GSTR-2B, it doesn’t wait for a tax officer to intervene. Instead, it sends an automated intimation. This is where you encounter Form DRC-01C, the official GST notice for traders India regarding this specific issue.

What is DRC-01C?

Form DRC-01C is a system-generated intimation, not a show-cause notice, sent to a taxpayer when their claimed ITC in GSTR-3B exceeds the available ITC in GSTR-2B by a pre-defined limit. This mechanism was formally introduced under Rule 88D of the CGST Rules to prompt taxpayers to self-regulate and either explain the difference or pay the excess tax claimed. The notice will be available in your GST portal dashboard and will clearly state the tax period in question and the exact amount of the discrepancy.

What Happens if You Ignore the Notice?

Ignoring a DRC-01C intimation is a serious mistake that can have cascading negative effects on your business operations. The system is designed to enforce compliance, and failure to respond will trigger automated consequences.

- Demand & Interest: The mismatched ITC amount is treated as tax that you have short-paid. You will be liable to pay this amount back to the government along with interest, which is currently calculated at a steep 18% per annum.

- Blockage of GSTR-1: This is the most severe consequence. If you fail to respond to the DRC-01C or fail to pay the amount you agree is due, the GST portal will block you from filing your GSTR-1 (or using the Invoice Furnishing Facility – IFF) for the subsequent tax period. This means you cannot generate e-way bills or issue tax invoices to your customers, effectively bringing your business to a standstill.

- Penalties: Continued non-compliance can lead to further departmental action, including the initiation of demand and recovery proceedings under Section 73 or 74 of the CGST Act, which can involve additional penalties. Understanding the Key Differences Between Sections 73 and 74 of the CGST Act in GST Demand Notices is crucial at this stage.

Your Step-by-Step Action Plan: An ITC Mismatch Guide

Receiving a notice can be stressful, but with a structured approach, it becomes a manageable task. Follow this plan on how to handle GST notices to ensure you respond effectively and protect your business. This systematic process forms the core of our ITC mismatch guide.

Step 1: Acknowledge and Analyze the Notice

The first rule is not to panic. Open the notice (Form DRC-01C, Part-A) on the GST portal. Read it carefully and note down three critical pieces of information:

- The specific tax period (e.g., January 2024).

- The exact discrepancy amount mentioned.

- The due date for your response, which is typically seven working days from the date you receive the intimation.

Step 2: The Reconciliation Process – Key Steps for ITC Matching

This is the most crucial part of your investigation. You need to dig into your records to find the source of the discrepancy.

- Log in to the official GST Portal.

- Navigate to the services tab and download your GSTR-2B for the relevant month.

- Export your purchase records from your accounting software (like Tally, Zoho, etc.) for the same period.

- Now, perform a line-by-line comparison. Place the GSTR-2B data and your purchase register side-by-side in a spreadsheet. Check for differences in invoice numbers, dates, GSTINs of suppliers, and tax amounts. This will help you pinpoint the exact invoices that are causing the mismatch.

Step 3: Communicate with Your Supplier

If your reconciliation reveals that the error is on your supplier’s end (e.g., they haven’t uploaded an invoice or have uploaded it with incorrect details), your next step is communication.

- Contact your supplier immediately via email or phone.

- Clearly provide them with the details of the missing or incorrect invoice.

- Request them to rectify the error in their next GSTR-1 filing. For example, they can add a missed invoice or amend an incorrect one.

- Crucially, keep a record of this communication (email trail, call logs) as it can be used as evidence in your reply to the department.

Step 4: Responding to the Notice (DRC-01C, Part-B)

After completing your analysis, you must file a reply in Part-B of Form DRC-01C on the GST portal. You have two primary paths to take:

- You Agree with the Discrepancy: If you find the mistake was yours (e.g., you claimed extra ITC by mistake), you must pay the excess amount claimed along with the applicable interest. This payment must be made using Form DRC-03. After making the payment, you will receive an Application Reference Number (ARN). You must mention this ARN in your reply in Part-B of DRC-01C as proof of payment.

- You Disagree with the Discrepancy: If you believe your claim is correct and there’s a valid reason for the mismatch, you must provide a clear and concise explanation in the reply box. Some valid reasons could be:

- “The discrepancy is due to a clerical error made while filing GSTR-3B. The excess ITC claimed of Rs. [Amount] will be reversed in the GSTR-3B for the upcoming tax period of [Month, Year].”

- “The mismatch is due to our supplier [Supplier Name, GSTIN] filing their GSTR-1 late. They have confirmed that the invoice will reflect in our GSTR-2B for [Month, Year]. Proof of communication with the supplier is attached.”

- “The ITC was claimed on an invoice from a supplier who files quarterly returns (QRMP). The credit is valid and will reflect once the supplier files their quarterly GSTR-1.”

Proactive Measures for Future Indian Traders GST Compliance

The best way to handle notices is to prevent them from being generated in the first place.

- Monthly Reconciliation: Do not wait for a notice. Make it a mandatory monthly business practice to reconcile your purchase records with your GSTR-2B before filing your GSTR-3B. Following the correct procedure is essential, as detailed in our guide on How to File GSTR-1 & GSTR-3B Correctly – Step-by-Step Guide 2025.

- Supplier Vetting: Before engaging with new suppliers, check their GST filing consistency on the GST portal. A supplier with a poor compliance history is a risk to your ITC.

- Maintain Impeccable Records: Keep organized digital and physical records of all your purchase invoices, payment proofs, and any important communications with your suppliers regarding GST matters.

Conclusion

An ITC mismatch notice between GSTR-2B and GSTR-3B is a serious compliance matter that should never be ignored. However, it is not a cause for alarm if handled systematically. The key to successful resolution lies in timely reconciliation, clear communication with your suppliers, and submitting a well-reasoned, evidence-backed response to any notice like DRC-01C. This ITC mismatch guide provides a clear roadmap, but remember that being proactive through diligent monthly checks is far better (and cheaper) than being reactive to department queries. By integrating these practices, you can ensure smooth Indian traders GST compliance and protect your business’s financial health.

Navigating GST notices and ensuring perfect compliance can be complex. If you need expert assistance in resolving GSTR-2B discrepancies or managing your GST filings, TaxRobo’s dedicated team is here to help. Contact us today for a hassle-free GST consultation!

Frequently Asked Questions (FAQs)

1. What is the time limit to respond to a DRC-01C notice for an ITC mismatch?

You are required to submit your reply in Part-B of Form DRC-01C or pay the disputed amount via DRC-03 within seven working days from the date the intimation is made available on the GST portal.

2. Can I claim ITC if an invoice is not showing in my GSTR-2B?

As per GST law (specifically Section 16(2)(aa) of the CGST Act), one of the mandatory conditions for claiming ITC is that the details of the corresponding invoice must be furnished by your supplier in their GSTR-1, which must then appear in your GSTR-2B. Claiming ITC for an invoice that is not reflected in your GSTR-2B is a direct violation and the primary reason for mismatch notices.

3. What should I do if my supplier corrects their mistake after I have already paid the demand in DRC-03?

If you have already paid the amount and interest to settle the notice, you have not lost the credit forever. Once your supplier corrects their return (e.g., amends the invoice or files their GSTR-1), the invoice will correctly appear in a subsequent month’s GSTR-2B. You can then reclaim that ITC in the GSTR-3B of that subsequent month. It is vital to maintain clear records to support this reclaim if questioned later.

4. Is it mandatory to use software for ITC reconciliation?

While it is not legally mandatory, using accounting or specialized reconciliation software is highly recommended for any growing business. Manual reconciliation using spreadsheets is prone to human error and becomes incredibly time-consuming as the number of invoices increases. Software automates the matching process, highlights discrepancies instantly, and saves significant time and effort. For businesses seeking a foolproof solution, professional services like those offered by TaxRobo provide an expert-led approach to ensure flawless compliance.