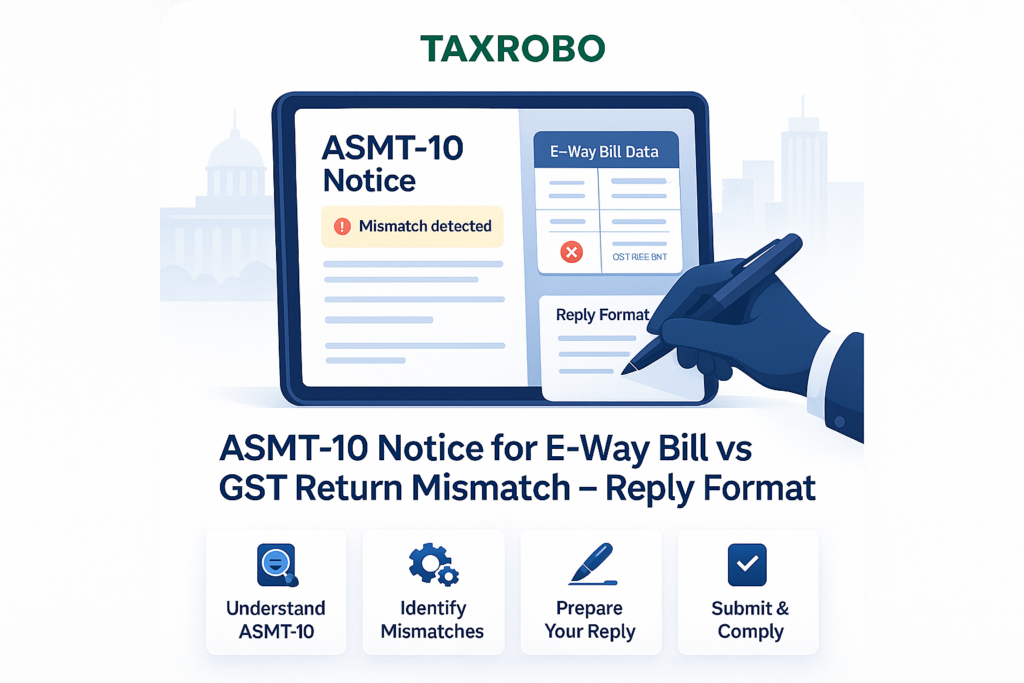

ASMT-10 Notice for E-Way Bill vs GST Return Mismatch – Reply Format

Receiving a notice from the GST department can be an intimidating experience for any business owner. The sight of Form ASMT-10, in particular, can cause immediate concern. However, this communication is often more manageable than it first appears. A common reason for this notice is a discrepancy between your E-Way Bill data and your GST returns, and understanding how to draft a proper reply is crucial. This comprehensive guide will walk you through everything you need to know about responding to an E-Way Bill mismatch notice, providing a clear format and actionable steps. A timely and well-documented reply can prevent further scrutiny, penalties, and legal complications, ensuring your business maintains good GST compliance for Indian businesses and stays on the right side of the law. This article will cover what the ASMT-10 notice is, common reasons for mismatches, a step-by-step reply process, and a sample reply format you can use.

What is an ASMT-10 Notice and Why Did You Receive It?

First and foremost, it’s important to understand that an ASMT-10 is a scrutiny notice, not a demand for tax payment. Think of it as an inquiry or a “please explain” letter from the GST officer. It is issued when the automated system on the GST portal or a tax officer identifies a potential discrepancy in GST returns India when compared with other available data. In this specific context, the notice is issued because the system has flagged inconsistencies between the outward supplies you declared in your GST returns (like GSTR-1 and GSTR-3B) and the data recorded in the E-Way Bills you generated during the same period.

This notice is issued under the authority of Section 61 of the Central Goods and Services Tax (CGST) Act, 2017, which allows a proper officer to scrutinize a registered person’s return and related particulars to verify its correctness. The primary purpose of these ASMT-10 Indian tax notices is to give you, the taxpayer, an opportunity to provide clarification and correct the record. It is a procedural step designed to promote transparency and self-correction before any more serious action, like an audit or investigation, is initiated. Receiving one means you need to act, but not panic.

Common Reasons for an E-Way Bill and GST Return Mismatch

Understanding the root cause of the notice is the first step toward resolving it. The E-Way Bill vs GST return issues highlighted in an ASMT-10 often stem from simple human errors or procedural gaps rather than intentional misreporting. A full understanding of the E-Way Bill: Meaning, Rules, & Online Generation can help prevent these errors. By identifying the likely cause, you can formulate a more accurate and effective reply. Here are some of the most common reasons for these mismatches.

Clerical and Typographical Errors

The simplest and most frequent cause is a manual error. A small mistake during data entry can easily trigger a mismatch. This includes:

- Incorrectly typing an invoice number or date.

- Entering the wrong GSTIN for the buyer or seller.

- Mistakes in the taxable value or tax amount (e.g., entering ₹60,000 instead of ₹6,000).

- These errors can happen on either the E-Way Bill portal or while filing the GSTR-1 return.

Timing Differences in Reporting

This is a common issue for transactions that occur near the end of a month. For example:

- You generate an E-Way Bill for goods shipped on the 30th of March.

- However, as per your accounting policy or due to a delay in finalising the sale, the invoice is officially recorded in your books and reported in your GSTR-1 for the next month, April.

- The GST system sees an E-Way Bill in March but no corresponding invoice in the March GSTR-1, leading to a mismatch.

Cancelled Transactions or Sales Returns

Business operations are dynamic, and not all planned transactions go through.

- Cancelled Orders: An E-Way Bill might be generated for a dispatch, but the customer cancels the order before the goods are delivered. If you fail to cancel the E-Way Bill within the stipulated 24-hour window, it remains active in the system, creating a discrepancy with your GSTR-1 which won’t show this sale.

- Sales Returns: A customer returns goods for which an E-Way Bill was generated. You issue a credit note to account for this return in your GSTR-1, but the original E-Way Bill data is not automatically adjusted, causing a mismatch between total outward supplies.

Incorrect Reporting of B2B vs. B2C Sales

The classification of sales is critical in GST. A mismatch can occur if:

- A Business-to-Business (B2B) transaction, which requires the buyer’s GSTIN, is mistakenly reported as a Business-to-Consumer (B2C) sale in GSTR-1.

- Conversely, a B2C sale might be incorrectly categorized as B2B. This error affects how the data is cross-referenced and can easily lead to a scrutiny notice.

Mismatch in HSN/SAC Codes or Tax Rates

Consistency is key. A discrepancy can arise if you:

- Use one HSN (Harmonized System of Nomenclature) code for a product while generating the E-Way Bill but use a different HSN code for the same product in your GSTR-1 return.

- Apply a different tax rate (e.g., 18% on the E-Way Bill but 12% in the GSTR-1) for the same supply due to an error.

A Step-by-Step Guide to Responding to an E-Way Bill Mismatch Notice

Once you understand the potential cause, formulating a response becomes a structured process. This ASMT-10 notice reply guide India provides a clear, step-by-step plan for preparing and submitting your clarification effectively. Following this process will ensure you address all the officer’s concerns and provide the necessary proof, increasing the likelihood of a swift resolution.

Step 1: Analyze the Notice Carefully

Do not skim through the notice. Read every line of the ASMT-10 document to understand exactly what the tax officer is questioning. The notice will typically contain a table or annexure that highlights the specific discrepancies, including the invoice numbers, dates, and amounts in question, along with the relevant tax periods. Make a note of every single query raised by the officer.

Step 2: Reconcile Your Data Internally

This is the most critical step in how to handle E-Way Bill mismatch. You need to become a detective and find the source of the discrepancy yourself.

- Go to the E-Way Bill portal and download a detailed report of all E-Way Bills generated for the period mentioned in the notice.

- Log in to the GST Portal and download your filed GSTR-1 and GSTR-3B data for the same period.

- Use a spreadsheet program like Microsoft Excel to compare these reports line-by-line. Create columns for E-Way Bill data and GSTR-1 data side-by-side to easily spot the differences in invoice numbers, dates, values, or GSTINs. This reconciliation sheet will form the backbone of your reply.

Step 3: Prepare a Detailed, Point-by-Point Clarification

Your reply must be submitted in Form GST ASMT-11. Do not write a generic, vague response. Instead, address each discrepancy noted in the ASMT-10 individually and systematically.

- For each point, first state the discrepancy as mentioned in the notice.

- Then, provide a clear, concise, and logical explanation for it. For instance, you could write: “Regarding the mismatch for Invoice No. INV-098, this was due to a typographical error where the taxable value was entered as Rs. 75,000 in the E-Way Bill portal instead of the correct value of Rs. 7,500. The correct value is accurately reflected in our GSTR-1. A copy of the original tax invoice is attached as Annexure-A for your reference.”

Step 4: Gather and Attach Supporting Documents

An explanation without evidence is just a claim. You must back up every point in your reply with documentary proof. Compile all relevant documents and create a single, consolidated PDF file for easy uploading. This file should include:

- A copy of the reconciliation statement you prepared in Step 2.

- Scanned copies of the relevant tax invoices.

- Copies of any credit notes or debit notes related to the transactions in question.

- Copies of the transporter’s consignment note or Lorry Receipt (LR copy).

- Any relevant communication with the buyer, such as emails confirming an order cancellation or goods return.

Step 5: File Your Reply (Form ASMT-11) on the GST Portal

Once your written clarification and supporting documents are ready, you need to file them online.

- Log in to the GST Portal with your credentials.

- Navigate to the following path: Services > User Services > View Additional Notices/Orders.

- Here you will find the ASMT-10 notice sent to you. Click on the “Reply” option next to it.

- This will open Form ASMT-11. You can type your reply directly in the text box or upload the reply you prepared on your letterhead.

- Use the upload option to attach the single PDF file containing all your supporting documents.

- Finally, file the reply using a Digital Signature Certificate (DSC) or Electronic Verification Code (EVC).

E-Way Bill Mismatch Notice Reply Format (ASMT-11 Template)

Using a professional and structured format for your reply is essential. Here is a template that you can adapt to create your E-Way Bill mismatch notice reply format. This should be prepared on your official company letterhead.

[Your Company Letterhead]

To,

The GST Officer,

[Jurisdiction/Address as mentioned in the notice]

Reference No (ARN): [Mention the ARN from ASMT-10]

Date of Notice: [Date mentioned on ASMT-10]

Subject: Reply to Scrutiny Notice in Form GST ASMT-10 regarding discrepancies between E-Way Bill data and GST Returns

Respected Sir/Madam,

This is with reference to the notice ASMT-10 issued to us, [Your Company Name], holding GSTIN [Your GSTIN], for the tax period [Mention Tax Period, e.g., April 2023 to June 2023]. We have carefully reviewed the discrepancies noted in the said notice and wish to provide the following point-wise clarifications for your kind consideration:

1. Discrepancy Noted: [Copy the first discrepancy exactly as written in the notice. E.g., “Mismatch in taxable value for Invoice No. 123 dated 15-05-2023.”]

Our Explanation: [Provide your clear, concise explanation. E.g., “This difference arose due to a timing mismatch. The E-Way Bill (No. XXXXX) was generated on 31st March 2023, while the corresponding invoice was accounted for in our GSTR-1 for April 2023 as per our standard accounting policy. The transaction is correctly reported in the subsequent tax period.”]

2. Discrepancy Noted: [Copy the second discrepancy from the notice. E.g., “E-Way Bill No. YYYYY generated but corresponding invoice not found in GSTR-1.”]

Our Explanation: [Provide your explanation. E.g., “The E-Way Bill (No. YYYYY) was generated for a supply that was subsequently cancelled by the customer due to quality issues. As the cancellation occurred after the 24-hour window, the E-Way bill could not be cancelled. A copy of the cancellation email from the customer and the corresponding credit note (No. CN-010) is attached herewith as evidence.”]

(Continue this format for all discrepancies listed in the notice)

To support our explanations, we have attached the following documents in a consolidated file:

- Detailed Reconciliation Statement showing the comparison between E-Way Bill data and GSTR-1.

- Copies of relevant Tax Invoices.

- Copies of relevant Credit Notes.

- Copies of transport documents (LR Copies).

We believe the above explanations and the enclosed documents satisfactorily clarify the discrepancies observed by your good office. We are committed to ensuring full compliance with GST regulations. We humbly request you to kindly review our submission and consider dropping the proceedings initiated via the said notice.

Thanking you,

For [Your Company Name]

[Authorized Signatory Name & Signature]

[Designation]

What to Expect After You File Your Reply

After you have filed your reply in Form ASMT-11, the ball is in the tax officer’s court. There are two primary outcomes:

- Scenario 1: The Officer is Satisfied: If your reply is comprehensive and the supporting documents are found to be satisfactory, the officer will accept your explanation. They will conclude the proceedings by issuing an order in Form GST ASMT-12, informing you that no further action is required. This is the ideal outcome.

- Scenario 2: The Officer is Not Satisfied: If the officer finds your explanation inadequate, the documents insufficient, or if you failed to pay any tax you admitted was short-paid, they may initiate further action. This could involve proceeding under Section 65 (Audit by tax authorities), Section 66 (Special Audit), or directly issuing a Show Cause Notice (SCN) under Section 73 (for non-fraud cases) or Section 74 (for fraud cases) to demand the tax along with interest and penalty. These actions often fall under specific legal sections, making it important to review guides like Understanding Section 73 of the CGST Act: Handling GST Demand Notices Without Fraud.

At this stage, resolving E-Way Bill and GST issues can become significantly more complex. If the matter escalates, it is highly advisable to seek professional help. The experts at TaxRobo can help you navigate these challenges, represent your case, and ensure a proper resolution.

Conclusion

An E-Way Bill mismatch notice in Form ASMT-10 is a common compliance check and should not be a cause for panic. It is an opportunity to rectify errors and demonstrate your commitment to transparent tax practices. The key to successfully resolving it lies in a methodical approach: timely analysis of the notice, careful internal reconciliation of data, preparing a detailed and documented reply, and filing it correctly on the GST portal. By being proactive and maintaining good records, you can handle such notices efficiently. This highlights The Importance of Accurate Record-Keeping to Prevent GST Demand Notices. Regular reconciliation of your E-Way Bills with your GSTR-1 filings is the best way to prevent such notices from being issued in the first place.

Feeling overwhelmed by GST notices and compliance tasks? Let TaxRobo’s team of seasoned experts handle your GST compliance, from regular filings to notice replies, so you can focus on what you do best—growing your business. Contact us today for a consultation!

FAQs

Q1. What is the time limit to reply to an ASMT-10 notice?

Answer: You are generally required to file your reply in Form ASMT-11 within 30 days from the date of service of the notice. However, the exact time limit will be specified in the notice itself, and it’s crucial to adhere to that deadline.

Q2. What happens if I ignore an E-Way Bill mismatch notice?

Answer: Ignoring an ASMT-10 is highly inadvisable. If no explanation is provided within the stipulated time, the tax officer will assume that you have nothing to say in your defense. They may proceed with determining your tax liability based on the information available to them and can initiate action under Section 73 or 74 of the CGST Act, which will likely result in a demand order for tax, interest, and penalties.

Q3. Do I need a Chartered Accountant (CA) or a tax consultant to reply to ASMT-10?

Answer: While it is not legally mandatory to hire a professional for simple clerical errors that you can easily explain and document, it is highly recommended for complex cases or large discrepancies. Tax experts can help prepare a legally sound, strategically worded reply with proper documentation, which significantly minimizes the risk of the notice escalating into a larger issue. This is a core part of TaxRobo’s GST return mismatch E-Way Bill solutions.

Q4. Is an ASMT-10 the same as a demand notice?

Answer: No, they are very different. An ASMT-10 is a pre-adjudication scrutiny notice that gives you an opportunity to explain a potential discrepancy. It does not demand any payment. A demand notice, such as one issued in Form DRC-07, is an adjudication order issued after the tax liability has been formally determined and confirmed by the officer. It demands the payment of a specific amount of tax, interest, and penalty. Replying properly and convincingly to an ASMT-10 is your best chance to prevent it from ever escalating to a demand notice.