What are the latest trends in bank loan documentation, including project and CMA reports?

Bank loans are often the lifeblood for small businesses aiming to expand or the key enabler for individuals looking to achieve significant personal goals like buying a home or funding education in India. However, securing these loans involves navigating the often complex and continuously evolving landscape of bank loan documentation. Requirements change, scrutiny levels shift, and staying updated can feel like a challenge in itself. This post dives into the latest trends in bank loan documentation, with a specific focus on how requirements for crucial documents like Project Reports and Credit Monitoring Arrangement (CMA) reports are changing in India. Understanding these bank loan documentation trends in India is no longer just helpful; it’s crucial for preparing a strong application that significantly improves your chances of loan approval.

The Shifting Landscape: Understanding Latest Trends in Bank Loan Documentation in India

From a bank’s perspective, loan documentation serves critical purposes: assessing the risk associated with lending, ensuring the borrower’s ability to repay, and complying with regulatory guidelines set by the Reserve Bank of India (RBI) and other authorities. The core objective remains the same – lending responsibly – but the methods and focus areas are evolving. The overall direction points towards increased scrutiny of financial health and projections, a significant move towards digitization of processes, and a stronger emphasis on verifiable compliance history. Understanding these latest trends in bank loan documentation India helps applicants align their preparations with current banking expectations, moving beyond simply submitting documents to presenting a compelling case for creditworthiness. Banks are increasingly leveraging technology and data analytics to make more informed lending decisions, meaning the quality, accuracy, and presentation of your documentation matter more than ever.

Key Trends Shaping Bank Loan Documentation Today

Navigating the loan application process requires awareness of the specific shifts happening right now. Several key trends are influencing how banks approach documentation and what they expect from applicants:

Trend 1: Increased Digitalisation and Automation

The move towards digital is undeniable. Banks across India are increasingly adopting online application portals, allowing borrowers to submit applications and supporting documents electronically. This includes the acceptance of scanned documents (PDFs), leveraging e-KYC (Know Your Customer) processes often linked with Aadhaar, and the growing use of legally valid digital signatures (like Aadhaar eSign or Dongle-based DSCs). Platforms like DigiLocker are also being integrated by some institutions for seamless document verification. The primary impact of this trend is the potential for faster processing times and reduced physical paperwork. However, it also necessitates that applicants have reliable internet access, basic digital literacy, and are comfortable using online platforms.

Actionable Insight: Familiarize yourself with online banking portals and digital document submission processes. Ensure you have clear scans of all necessary documents and explore setting up a DigiLocker account if you haven’t already.

Trend 2: Enhanced Scrutiny on Financial Viability & Projections (Project Reports Focus)

Gone are the days when basic financial projections were sufficient, especially for business loans. Banks are now applying enhanced scrutiny to the financial viability presented in project reports. They are looking beyond the surface numbers, demanding realistic and well-researched market analysis, thorough competitor assessments, and robust financial projections. This means your revenue forecasts, cost breakdowns (clearly distinguishing fixed and variable costs), break-even analysis, projected Profit & Loss statements, Balance Sheets, and Cash Flow statements need to be credible and justifiable. Lenders are increasingly wary of overly optimistic or unsupported figures. The impact is clear: businesses need more detailed, data-backed, and meticulously prepared project reports for bank loans India. The quality of your bank loan documentation project reports India can significantly influence the lender’s perception of your business acumen and the project’s feasibility.

Trend 3: Greater Reliance on Comprehensive CMA Reports

For existing businesses seeking working capital loans, term loans, or enhancement of credit limits, the Credit Monitoring Arrangement (CMA) report is paramount. CMA data typically includes analysis of past financial performance (usually 3-5 years) and projections for the future (usually 3-5 years). The key trend here is the increased rigor with which banks are analysing CMA data to assess repayment capacity, operational efficiency, and overall financial discipline. Simple submission is not enough; banks are diving deep into ratio analysis derived from the CMA data. Critical ratios related to liquidity, leverage, profitability, and efficiency are being meticulously examined. The impact is a pressing need for accurate, detailed, and well-structured CMA reports that truly reflect the financial health and trajectory of the business. Understanding the current CMA reports trends in India is vital for businesses needing ongoing credit facilities.

Trend 4: Stronger Emphasis on Regulatory Compliance History

A clear indicator of financial discipline and business stability for banks is a clean regulatory compliance record. Increasingly, banks are making the verification of timely Goods and Services Tax (GST) filings (like GSTR-1 and GSTR-3B) and Income Tax Returns (ITR) a standard part of their due diligence. Consistent, on-time filings are viewed positively, suggesting responsible financial management. Conversely, delays, non-filing, or significant discrepancies can raise red flags and negatively impact loan approval chances, even if other parameters seem acceptable.

Actionable Insight: Prioritize maintaining impeccable tax records. Ensure all GST returns and ITRs are filed accurately and within deadlines. You can access official portals for information:

- GST Portal: https://www.gst.gov.in/

- Income Tax Department: https://www.incometax.gov.in/

Consistent compliance is non-negotiable in the current lending environment. Consider using professional services like TaxRobo GST Service or TaxRobo Income Tax Service to ensure accuracy and timeliness.

Trend 5: Standardisation vs. Customisation

There’s a dual trend emerging regarding documentation requirements. For smaller ticket loans, particularly standardized products like personal loans, vehicle loans, or specific government schemes like MUDRA loans, banks are moving towards greater standardisation in documentation checklists. This often involves simpler forms and leveraging digital processes extensively. However, for larger business loans, project financing, or complex working capital arrangements, the trend leans towards more customized and detailed documentation. Lenders require in-depth information tailored to the specific business, industry, and loan purpose. Requirements also naturally differ between salaried individuals (focus on income proof, credit score, KYC) and businesses (focus on financials, project reports/CMA, compliance, collateral).

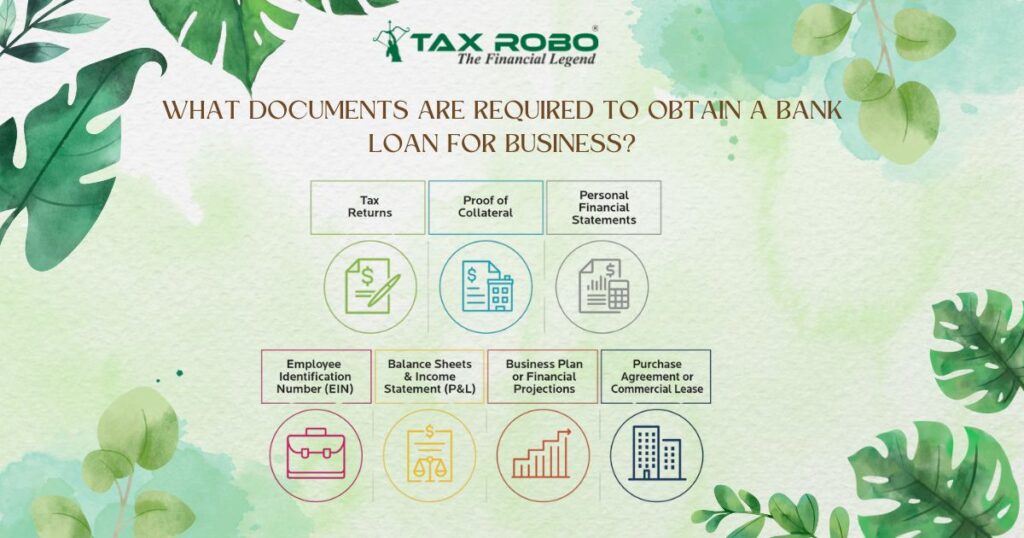

Deep Dive: Project Reports for Bank Loans India – What Lenders Focus On Now

Project reports are fundamental for businesses seeking loans for new ventures, expansions, or diversification. As part of the evolving bank loan documentation project reports India landscape, lenders are scrutinizing these documents more closely than ever. Simply outlining an idea is insufficient; banks want to see a viable, well-thought-out business plan backed by solid data. Understanding the current expectations for project reports for bank loans India is key to securing funding. Understanding What is a bank project report and why is it required for a business loan? is the first step.

Key Components Under Closer Scrutiny:

Banks are paying particular attention to the following aspects within project reports:

- Market Analysis: Lenders expect more than just generic statements. They want to see evidence of in-depth research covering the target market size, specific customer demographics, psychographics, a realistic assessment of existing competition (including their strengths and weaknesses), a clear SWOT (Strengths, Weaknesses, Opportunities, Threats) analysis for your venture, and a well-defined marketing and sales strategy. Primary research findings often carry more weight than secondary data alone.

- Financial Projections: This remains a cornerstone, but the emphasis is on realism and detail. Revenue forecasts must be logically derived and clearly linked to market size and sales strategy. Cost breakdowns should meticulously detail both fixed and variable costs, including assumptions used. An accurate break-even analysis is critical. Furthermore, banks expect comprehensive projected Profit & Loss Accounts, Balance Sheets, and Cash Flow statements, typically for the next 3-5 years (or longer, depending on the loan tenure). Sensitivity analysis, showing how projections change under different scenarios (e.g., lower sales, higher costs), adds significant credibility.

- Risk Assessment and Mitigation: Identifying potential risks is only half the battle. Banks want to see that you have realistically assessed potential challenges – market risks (e.g., changing customer preferences, new competitors), operational risks (e.g., supply chain disruptions, technology failures), and financial risks (e.g., interest rate hikes, cash flow shortages) – and have developed clear, actionable mitigation strategies for each significant risk.

- Implementation Plan: A vague timeline is no longer acceptable. Lenders look for a clear, phased implementation plan with specific milestones, timelines, and responsible parties for key activities related to project setup and execution.

Common Pitfalls Banks Are Watching For:

Lenders are increasingly adept at spotting weaknesses in project reports. Avoid these common pitfalls:

- Lack of Primary Research: Relying solely on generic industry reports without specific market validation.

- Unrealistic Assumptions: Overly optimistic revenue projections or underestimated costs without clear justification.

- Poor Structure and Clarity: Disorganized reports that are difficult to follow or lack essential details.

- Inconsistencies: Discrepancies between the narrative sections (like market analysis or operational plan) and the financial projections.

- Ignoring Key Risks: Failing to identify or adequately address potential business risks.

- Insufficient Promoters’ Contribution: Lack of adequate equity infusion from the business owners, indicating lower commitment.

Understanding Current CMA Reports Trends in India

For established businesses applying for loans or credit limit renewals, the Credit Monitoring Arrangement (CMA) report is a critical piece of documentation. The CMA reports trends in India clearly indicate that banks are relying more heavily on this data for deeper financial analysis rather than just as a formality. CMA data provides a historical perspective and future outlook, allowing banks to gauge performance consistency and future repayment ability. Understanding What is a CMA report and how does it support a bank loan application? is crucial for applicants.

Focus on Key Financial Ratios:

Banks are intensely analysing key financial ratios derived from CMA data to assess different facets of a business’s health. Understanding these ratios and what they signify is crucial:

| Ratio Category | Key Ratios Examples | What it Measures | Why Banks Focus on It |

|---|---|---|---|

| Liquidity | Current Ratio, Quick Ratio | Ability to meet short-term obligations | Ensures the business can pay its immediate debts without stress. |

| Leverage | Debt-to-Equity Ratio, Total Debt Ratio | Extent of debt financing vs. equity | Assesses financial risk; high leverage can mean higher risk for the lender. |

| Repayment Capacity | Debt Service Coverage Ratio (DSCR) | Ability to cover debt payments from operating income | Directly indicates if the business generates enough cash to repay the proposed loan. |

| Efficiency | Inventory Turnover, Debtors Turnover | How efficiently assets are used to generate sales | Shows operational effectiveness in managing stock and collecting receivables. |

| Profitability | Gross Profit Margin, Net Profit Margin | Overall profitability at different levels | Indicates the business’s ability to generate profit from its operations and manage costs. |

Banks analyze the trends in these ratios over time (past performance) and compare projected ratios against industry benchmarks. Significant deviations or negative trends require strong justification.

Data Accuracy and Verification:

Another significant trend is the increased emphasis on data accuracy and verification. Banks are no longer taking CMA data at face value. They are actively cross-verifying the figures presented in the CMA report with:

- Audited Financial Statements: Ensuring consistency with finalised, audited accounts.

- GST Returns: Comparing reported turnover in CMA with GST filings to check for discrepancies.

- Bank Statements: Verifying cash flows, sales receipts, and major expense payments against actual bank transactions.

Consistency across all financial documentation is paramount. Any discrepancies can lead to queries, delays, or even rejection of the loan application. This necessitates meticulous preparation of CMA data, ensuring it aligns perfectly with other financial records. Employing robust accounting practices is essential. Consider using TaxRobo Accounts Service to maintain accurate books that facilitate seamless CMA preparation.

Preparing Your Application: Navigating the Latest Trends in Bank Loan Documentation

Adapting to the current banking environment requires proactive preparation. Here are actionable tips to help you navigate the latest trends in bank loan documentation:

Maintain Pristine Financial Records:

This is the foundation. Implement robust accounting and bookkeeping practices from day one (or clean them up now). Ensure timely and accurate filing of all statutory returns, including GST and Income Tax. Organized, up-to-date financial records make documentation preparation significantly easier and demonstrate financial discipline to lenders. Understanding the importance of Maintaining Accurate Accounting Records for Tax Purposes is key.

Research Specific Bank Requirements:

While trends provide a general direction, specific documentation checklists can still vary slightly between banks and loan products. Always visit the official website of the bank you plan to apply to or speak directly with a loan officer to get their most current and specific checklist. Don’t rely solely on generic information.

Prepare Thorough and Realistic Reports:

Whether it’s a Project Report for a new venture or CMA data for an existing business, invest the necessary time and effort (or seek professional help) to create detailed, credible, and well-supported reports. Focus on realistic projections, thorough market analysis, clear risk mitigation, and consistency across all data points. Quality documentation speaks volumes.

Embrace Digital Processes:

Be prepared for the digital shift. Have readily available clear digital copies (scans/PDFs) of all required documents (ID proofs, address proofs, financial statements, tax returns, property papers, etc.). Familiarize yourself with online application forms and be ready for potential e-KYC or digital signature requirements.

Seek Professional Assistance:

Preparing comprehensive and compliant loan documentation, especially detailed project reports and accurate CMA data analysis, can be complex and time-consuming. If you feel overwhelmed or want to ensure your application aligns perfectly with the latest trends in bank loan documentation, consider seeking expert help. Firms like TaxRobo specialize in assisting businesses and individuals with meticulous documentation preparation, including insightful project reports and rigorous CMA data analysis, significantly strengthening your loan application. You can explore options like TaxRobo Online CA Consultation Service to discuss your specific needs.

Conclusion

The landscape of bank loan documentation in India is clearly evolving. Key takeaways regarding the latest trends in bank loan documentation include a strong push towards digitalisation, significantly enhanced scrutiny on financial projections within project reports, a more rigorous analysis of CMA data and key ratios, and an unwavering focus on regulatory compliance history.

Understanding and proactively adapting to these shifts is no longer optional for loan applicants – it’s essential for success. By maintaining clean financial records, preparing thorough and realistic documentation, embracing digital processes, and understanding exactly what lenders are looking for today, you can significantly improve your chances of securing the funds needed for your business growth or personal aspirations. Remember, a well-prepared application reflecting awareness of the current latest trends in bank loan documentation presents you as a credible and low-risk borrower.

If navigating these requirements seems daunting, or if you want expert assistance in preparing compelling project reports, accurate CMA data, or ensuring your overall loan documentation package is top-notch, don’t hesitate to reach out. Contact TaxRobo today for professional guidance tailored to the latest banking standards.

FAQs (Frequently Asked Questions)

Q1: What is the primary difference between a Project Report and a CMA Report for bank loans in India?

Answer: A Project Report is typically prepared for new business ventures or significant expansions. It outlines the business plan, market feasibility, technical details, and projected financials from scratch. A CMA Report, on the other hand, is usually required for existing businesses seeking loans or enhancement of credit limits. It analyses the company’s past financial performance (typically 3-5 years) and provides financial projections for the future (usually 3-5 years), focusing on demonstrating repayment capacity based on operational history.

Q2: Are digital signatures legally accepted for all bank loan documents in India?

Answer: The acceptance of digital signatures (like Aadhaar-based eSign or Dongle-based DSCs) is widespread and rapidly growing for bank loan documentation, governed by the Information Technology Act, 2000. Most banks accept them for application forms and various agreements. However, specific policies might vary slightly, especially for certain critical documents like property mortgage deeds in some states. It’s always best to confirm the specific bank’s policy for the type of loan and document in question.

Q3: How detailed does the market analysis in a project report need to be for the `latest trends in bank loan documentation`?

Answer: According to the latest trends in bank loan documentation, market analysis needs to be increasingly detailed and specific. Generic statements are insufficient. Banks expect quantifiable data on target market size, clear demographic/psychographic profiles of customers, thorough analysis of key competitors (products, pricing, market share, strengths, weaknesses), a practical SWOT analysis for the proposed venture, and a concrete marketing and sales strategy. Evidence of primary research often strengthens the analysis significantly.

Q4: Do salaried individuals applying for home loans or personal loans need Project/CMA reports?

Answer: Generally, no. Project Reports and CMA Reports are primarily requirements for business loans (like term loans, working capital finance, project finance). Salaried individuals applying for retail loans like home loans or personal loans typically need to provide documentation focusing on their income stability, credit history, and identity/address verification. This usually includes salary slips, Form 16, Income Tax Returns (ITR), bank account statements, KYC documents (PAN, Aadhaar), and potentially property documents for home loans.

Q5: Where can I find the absolute latest documentation checklist for a specific bank?

Answer: The most reliable and up-to-date source for a specific bank’s loan documentation checklist is the bank’s official website. Look for the section related to the specific loan product you are interested in (e.g., Business Loan, Home Loan). Alternatively, contacting a loan officer at the bank branch directly is highly recommended, as they can provide the latest requirements and clarify any doubts based on your specific profile and loan needs.