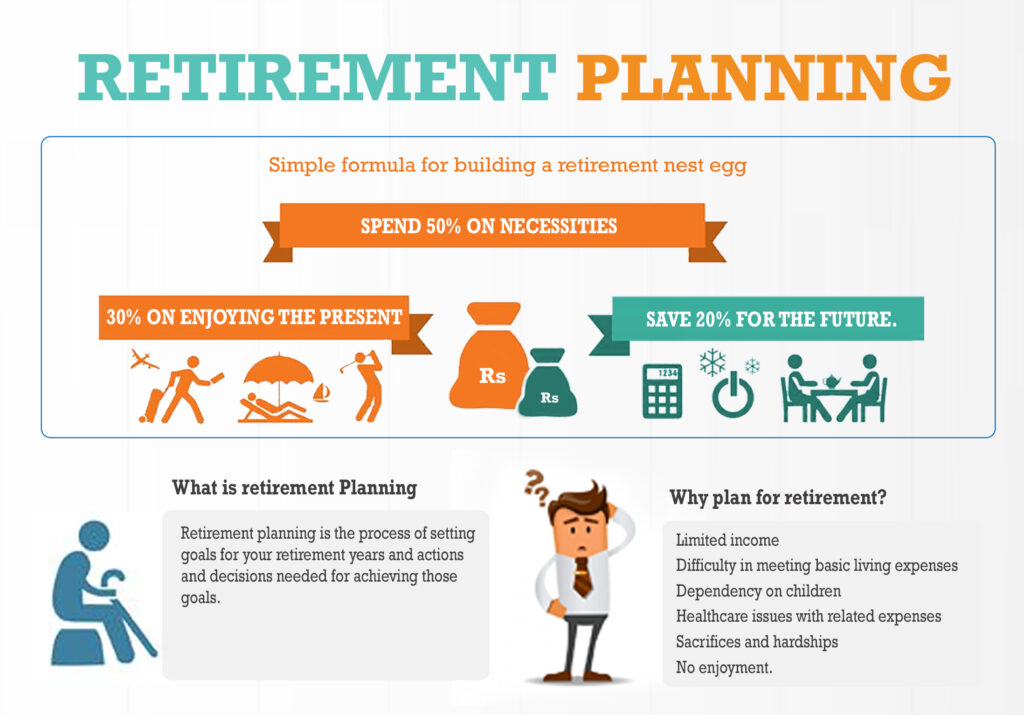

How do I plan for retirement through personal financial planning?

Imagine a future where work is optional, and your days are filled with pursuing passions, traveling, or simply relaxing, without the constant worry about bills. This vision of financial freedom in your golden years isn’t just a dream; it’s an achievable reality through careful and deliberate action. The key lies in proactive personal financial planning, specifically focused on building a secure future. Understanding What is financial planning and why is it important for individuals and corporations? is the first step. Especially in today’s dynamic environment, understanding how to plan for retirement in India is more critical than ever. Factors like rising inflation gradually eating away at savings, escalating healthcare costs, and significantly increased life expectancy mean that relying solely on chance or traditional support systems is no longer viable. Therefore, starting to plan for retirement early is not just advisable; it’s essential for long-term security and peace of mind.

This blog post aims to serve as your comprehensive guide, providing a clear roadmap and actionable personal financial planning tips India. Whether you are a salaried professional diligently building your career or a determined small business owner navigating the entrepreneurial landscape, the principles discussed here will help you create a robust strategy. We will delve into why starting early is paramount, outline a step-by-step process for creating your retirement blueprint, highlight common pitfalls to avoid, and explore various investment avenues suitable for the Indian context. Embarking on retirement planning in India is a journey, and this guide provides the essential framework to navigate it successfully, ensuring your later years are comfortable and worry-free.

Why is it Crucial to Plan for Retirement Early in India?

Timing is arguably the most significant factor when you plan for retirement. Starting early doesn’t just mean having more time to save; it means unlocking the power of compounding, effectively managing long-term risks like inflation and healthcare costs, and preparing for a longer post-retirement life. Delaying this crucial aspect of personal financial planning can significantly increase the effort required later and may even compromise your retirement goals. Let’s explore the specific reasons why early retirement planning in India is non-negotiable.

The Magic of Compounding

Compound interest is often called the eighth wonder of the world, and for good reason. It’s the process where your investment earnings start generating their own earnings. When you start saving and investing early, even small amounts can grow substantially over decades. Consider this simple illustration:

- Anjali starts investing ₹5,000 per month at age 25. Assuming a 12% average annual return, by age 60 (35 years of investing), her corpus could grow to approximately ₹3.28 Crores.

- Ajay starts investing the same ₹5,000 per month but begins at age 35. Assuming the same 12% return, by age 60 (25 years of investing), his corpus would be around ₹95 Lakhs.

Anjali’s 10-year head start allows her corpus to become nearly 3.5 times larger than Ajay’s, even though her total investment was only ₹6 Lakhs more (₹5000 * 12 * 10). This demonstrates the exponential power of time in investing. Leveraging compounding is one of the most fundamental retirement savings strategies for Indians; the earlier you begin, the less you need to save each month to reach your goal, and the more work your money does for you.

Tackling Inflation and Rising Healthcare Costs

Inflation is the silent wealth eroder. The price of goods and services tends to increase over time, meaning the value of your money decreases. What costs ₹100 today might cost ₹500 or more by the time you retire in 20-30 years. If your retirement savings don’t grow at a rate significantly higher than inflation, your purchasing power in retirement will be severely diminished. For example, monthly expenses of ₹50,000 today could easily balloon to over ₹2.5 Lakhs per month in 30 years, assuming an average inflation rate of 6%. Effective financial planning for retirement in India must explicitly account for this erosion.

Furthermore, healthcare costs in India are rising at an alarming rate, often outpacing general inflation. As you age, the likelihood of needing medical care increases. Planning for these potential expenses is a critical component of retirement fund planning India. Failing to adequately budget for healthcare can quickly deplete your retirement savings, forcing difficult choices in your later years. Starting early allows you to build a larger corpus that can comfortably accommodate both lifestyle expenses and unforeseen medical costs, adjusted for future inflation.

Increased Longevity & Changing Family Dynamics

Thanks to advancements in healthcare and better living standards, people in India are living longer than ever before. While a longer life is a blessing, it also means your retirement savings need to last longer – potentially 25, 30, or even more years post-retirement. This necessitates building a significantly larger retirement nest egg than previous generations required. Relying on guesswork or outdated assumptions about lifespan can lead to outliving your savings, a situation everyone wants to avoid.

Simultaneously, traditional family structures are evolving. The prevalence of joint families, where multiple generations lived together and provided mutual support, is declining. Nuclear families are becoming the norm, and children often move to different cities or countries for career opportunities. This shift increases the importance of financial self-reliance in retirement. You cannot solely depend on family support; building your own robust retirement fund through disciplined personal financial planning is essential for maintaining independence and dignity throughout your later years. Early planning ensures you have sufficient time to accumulate the substantial corpus needed for a long and independent retirement.

Step-by-Step Guide: How to Plan for Retirement Using Personal Financial Planning

Knowing why you need to plan is the first step; knowing how is the next crucial phase. A structured approach transforms the seemingly daunting task of retirement planning into manageable actions. This step-by-step guide breaks down the process, integrating key aspects of personal financial planning specifically tailored for individuals aiming to plan for retirement in India. Following these steps provides a clear pathway towards building the financial security you desire for your future.

Step 1: Define Your Retirement Vision & Goals

Before crunching numbers, you need a clear picture of what retirement looks like for you. This isn’t just about finances; it’s about your life.

- Action Point: Visualize your ideal retirement. Do you see yourself traveling extensively, pursuing hobbies like gardening or painting, spending more time with family, relocating to a quieter town, or perhaps doing some part-time consulting? The more detailed your vision, the better you can estimate the associated costs.

- Action Point: Decide on your target retirement age. The standard age is often 60, but you might aspire to retire earlier (say, 55) or plan to work longer (maybe 65). This decision significantly impacts the time horizon for your savings and the duration your corpus needs to last.

- Action Point: Estimate your likely annual expenses in retirement, based on your envisioned lifestyle, using today’s monetary value. Think about housing (will your mortgage be paid off?), food, utilities, travel, entertainment, healthcare, hobbies, and potential support for dependents. Don’t worry about inflation just yet; we’ll adjust for that later. But having a baseline figure in today’s terms is critical.

Clearly defining these elements forms the bedrock of effective financial planning for retirement in India. Without knowing your destination (your retirement goals), you cannot chart the course (your savings and investment strategy).

Step 2: Assess Your Current Financial Health

Once you know where you want to go, you need to understand your starting point. This involves taking a candid look at your current financial situation.

- Action Point: Calculate your current net worth. List all your assets – savings account balances, fixed deposits, mutual fund holdings, stocks, EPF/PPF balances, real estate value (be realistic), gold, etc. Then, list all your liabilities – home loan outstanding, car loan, personal loans, credit card debt, etc. Your net worth is your Total Assets minus your Total Liabilities. This gives you a snapshot of your financial standing today.

- Action Point: Track your monthly income and expenses diligently for a few months. Understand exactly where your money comes from and where it goes. This will reveal your current saving capacity – the difference between your income and expenses. Identifying areas where you can potentially cut back can free up more funds for retirement savings.

- Action Point: Compile a detailed list of all your existing investments specifically earmarked (even loosely) for long-term goals like retirement. Note down the current value, asset type (equity, debt, real estate), and where they are held (e.g., EPF statement, Demat account, MF statements, PPF passbook).

This assessment is fundamental to personal finance management for retirement in India. It provides clarity on your resources, spending habits, and existing provisions, forming the basis for calculating how much more you need to save.

Step 3: Calculate Your Target Retirement Corpus

Now it’s time to estimate the big number: how much money you’ll actually need when you retire. This is the cornerstone of retirement fund planning India.

- Method 1: Expense Method (Inflation-Adjusted):

- Take the estimated annual expenses in today’s terms (from Step 1).

- Project these expenses forward to your retirement age using an assumed average inflation rate (e.g., 5-6% per annum is often used for long-term planning in India). A future value calculator can help here. Let’s call this

Annual Expenses at Retirement. - Estimate the expected rate of return on your investments after retirement (post-tax, usually assumed to be conservative, e.g., 7-8%).

- Estimate the long-term inflation rate during your retirement (e.g., 5-6%).

- The target corpus =

[Annual Expenses at Retirement] / (Expected Rate of Return - Inflation Rate). For example, if your inflation-adjusted annual expense at retirement is ₹15 Lakhs, your expected return is 8%, and expected inflation is 6%, your target corpus is ₹15,00,000 / (0.08 – 0.06) = ₹7.5 Crores.

- Method 2: The ‘4% Rule’ Guideline: This rule suggests you can safely withdraw 4% of your initial retirement corpus each year (adjusting subsequent withdrawals for inflation) with a high probability of your money lasting 30 years. To use this, estimate your first year’s inflation-adjusted expenses in retirement and multiply by 25 (since 100/4 = 25). Example: If first-year expenses are ₹15 Lakhs, target corpus ≈ ₹15 Lakhs * 25 = ₹3.75 Crores. Caveat: This rule originated in the US market and might be too aggressive for India due to potentially different inflation and return dynamics. Use it as a rough check, not a primary calculation method.

- Action Point: Crucially, always use inflation-adjusted calculations. Ignoring inflation is one of the biggest retirement planning mistakes. Online retirement calculators available on many financial websites can simplify these calculations, but understand the assumptions they use (inflation rate, life expectancy, rate of return).

Subtract your current retirement-oriented savings (from Step 2) from this target corpus to determine the shortfall you need to cover through future savings and investments.

Step 4: Create Your Savings & Investment Strategy

With your target corpus defined and your current status assessed, you can now build your action plan. This involves figuring out how much to save regularly and where to invest it.

- Action Point: Determine the required monthly or annual savings amount. Use a financial goal calculator (available online) or work with an advisor. Input your target corpus shortfall, the number of years until retirement, and an expected rate of return on your future investments (be realistic, perhaps 10-12% p.a. for a long-term balanced portfolio). The calculator will show the Systematic Investment Plan (SIP) or lump sum amount needed. Commit to saving this amount consistently.

- Discuss various investment avenues suitable for retirement planning in India:

- Employee Provident Fund (EPF) / Voluntary Provident Fund (VPF): Primarily for salaried individuals. Mandatory contribution (12% of basic + DA) from employee and employer goes into EPF. Offers tax-free interest (currently 8.25% for FY24) and withdrawal upon retirement (subject to conditions). VPF allows voluntary additional contributions up to 100% of Basic + DA, earning the same EPF interest. It’s a safe, debt-oriented foundation.

- Public Provident Fund (PPF): Accessible to all residents. Offers EEE (Exempt-Exempt-Exempt) tax status – contributions (up to ₹1.5 Lakh/year under Sec 80C), interest earned, and maturity amount are all tax-free. Has a 15-year lock-in, extendable in 5-year blocks. Interest rate is set quarterly by the government (currently 7.1% p.a.). Excellent for safe, long-term, tax-efficient debt allocation.

- National Pension System (NPS): Government-backed scheme open to all citizens (18-70 years). Offers Tier I (mandatory lock-in till 60, primary retirement account) and Tier II (voluntary, withdrawable). Provides tax benefits under Sec 80CCD(1) (within 80C limit), exclusive deduction up to ₹50,000 under Sec 80CCD(1B), and employer contribution benefit (Sec 80CCD(2)). Offers choice of investment mix (Equity, Corporate Debt, Govt Securities) through Auto (age-based) or Active choice. Upon maturity (age 60), minimum 40% must be used to buy an annuity (provides regular pension), rest can be withdrawn lump sum (currently 60% is tax-free). Visit the official NPS Trust website for details.

- Mutual Funds (via SIPs): Offer diversification and professional management. Suitable for long-term wealth creation.

- Equity Funds: Invest primarily in stocks. High growth potential over the long term, but higher risk. Ideal for younger investors with a long time horizon. Includes Large-cap, Mid-cap, Small-cap, Flexi-cap, and ELSS (Equity Linked Savings Scheme, offers 80C benefit with 3-year lock-in).

- Debt Funds: Invest in bonds, government securities. Lower risk, aim for stable returns. Suitable for capital preservation, closer to retirement.

- Hybrid Funds: Invest in a mix of equity and debt. Balance risk and return. Good for moderate risk appetite.

- Systematic Investment Plans (SIPs): Allow regular, disciplined investment (e.g., monthly) in mutual funds, benefiting from rupee cost averaging.

- Direct Equity: Investing directly in stocks. Offers potential for high returns but requires significant knowledge, research, and risk appetite. Suitable only for informed investors.

- Other Options:

- Real Estate: Can provide rental income and capital appreciation but lacks liquidity and involves high transaction costs. Consider if it fits your overall plan.

- Gold: Often seen as an inflation hedge. Sovereign Gold Bonds (SGBs) are a tax-efficient way to invest in gold digitally, offering interest and tax-free redemption on maturity.

- Action Point: Diversify your investments across asset classes (equity, debt, gold, etc.) and within asset classes (different types of mutual funds or stocks). Asset allocation is key – tailor the mix based on your risk tolerance and age. Younger investors can typically afford higher equity exposure for growth, gradually shifting towards safer debt instruments as retirement approaches to protect the accumulated corpus. This forms a core part of retirement savings strategies for Indians.

Step 5: Integrate Tax Planning

Efficient tax planning is crucial to maximize your effective returns and ensure more of your money works towards your retirement goal. Understanding the tax treatment of different investment options is vital.

- Tax Treatment Categories: Investments generally fall into these categories regarding taxation:

- EEE (Exempt-Exempt-Exempt): Contribution (investment), Accumulation (interest/growth), and Withdrawal (maturity) are all tax-free. Examples: EPF, PPF, Sukanya Samriddhi Yojana, SGB (if held till maturity).

- EET (Exempt-Exempt-Taxable): Contribution and Accumulation are tax-free/deductible, but Withdrawal/Maturity amount is taxable. Example: NPS (partially, as 60% lump sum withdrawal is tax-free, but annuity income is taxed).

- TEE (Taxable-Exempt-Exempt): Contribution is made from post-tax income, Accumulation is tax-free/exempt, and Withdrawal is tax-free. Example: Often cited for ULIPs but specific conditions apply.

- TTE (Taxable-Taxable-Exempt) / TTT (Taxable-Taxable-Taxable): Less favorable. Bank FDs, for instance, are often TTT (investment from post-tax income, interest taxed annually, maturity amount includes taxed interest). Equity Mutual Funds/Stocks held > 1 year have LTCG tax (currently 10% above ₹1 Lakh gain).

- Leverage Tax Deductions: Utilize specific sections of the Income Tax Act designed to encourage retirement savings:

- Section 80C: Allows deduction up to ₹1.5 Lakhs for investments in EPF, PPF, ELSS, NPS (Tier I employee contribution), life insurance premiums, etc.

- Section 80CCD(1B): Allows an additional deduction of up to ₹50,000 specifically for contributions to NPS Tier I, over and above the 80C limit.

- Section 80CCD(2): Allows deduction for employer’s contribution to employee’s NPS account (up to 10% of salary for private-sector, 14% for government employees).

- For the latest rules and limits, always refer to the official Income Tax Department website.

- Maximize Effective Returns: Choosing tax-efficient instruments like PPF, EPF, NPS, ELSS (considering LTCG), and SGBs can significantly boost your net returns over the long run compared to fully taxable options like traditional bank FDs or bonds, helping your retirement corpus grow faster. Explore some of the Top Tax-Saving Investment Options in India to understand these better.

Integrating tax considerations into your investment choices from the beginning is a hallmark of smart personal financial planning for retirement.

Step 6: Monitor, Review, and Rebalance

Creating a retirement plan is not a one-time event. Life circumstances change, markets fluctuate, and regulations evolve. Regular monitoring and adjustments are essential to keep your plan on track.

- Action Point: Schedule a review of your retirement plan at least once a year. Check your progress against your savings goals. Assess investment performance. Re-evaluate your assumptions (inflation, expected returns, retirement age). Also, conduct a review after significant life events like marriage, childbirth, a major salary increase or decrease, job change, or receiving an inheritance.

- Rebalance Your Portfolio: Over time, due to differing returns, your asset allocation mix will drift from your target (e.g., equities might grow faster and become a larger percentage than intended). Rebalancing involves selling some of the outperforming assets and buying more of the underperforming ones to bring your portfolio back to its desired allocation (e.g., back to 70% equity, 30% debt). This helps manage risk and potentially enhances long-term returns by forcing you to “sell high, buy low”.

- Adjust Contributions: If your income increases, aim to increase your retirement savings contributions proportionally, or even more, to accelerate your progress. If you face a temporary setback, try to maintain contributions if possible, but adjust your plan realistically if needed. If your goals change (e.g., you decide to retire earlier or want a more luxurious retirement), recalculate your required savings and adjust accordingly.

Consistent monitoring and disciplined adjustments ensure your retirement planning in India remains relevant and effective throughout your working life, adapting to changes and keeping you directed towards your ultimate financial goals.

Common Mistakes to Avoid When You Plan for Retirement in India

While the steps provide a roadmap, navigating the path to retirement security requires avoiding common pitfalls that can derail even well-intentioned plans. Being aware of these mistakes can help you stay vigilant and make more informed decisions as you plan for retirement in India. Recognizing these traps is a key part of personal finance management for retirement in India.

Delaying the Start

This is arguably the most damaging mistake. As illustrated earlier with the power of compounding, every year of delay significantly increases the amount you need to save later to reach the same goal. Procrastination is expensive. Thinking “I’ll start saving seriously next year” or “once I get a promotion” means losing valuable time where your money could be growing exponentially. The best time to start planning and saving for retirement was yesterday; the second-best time is today.

Underestimating Inflation

Many people calculate their retirement needs based on today’s expenses without adequately factoring in the long-term impact of inflation. A corpus that seems sufficient now might cover less than half of your actual needs 20 or 30 years down the line. Always use an inflation-adjusted calculation (as described in Step 3) for estimating your target corpus and future expenses. Failing to do so is setting yourself up for a potential shortfall in your retirement years.

Ignoring Healthcare Expenses

Healthcare costs often rise faster than general inflation and can constitute a significant portion of expenses in later life. Simply assuming your regular retirement corpus will cover medical emergencies or chronic conditions is risky. It’s prudent to specifically account for healthcare, either by building a larger overall corpus, earmarking a separate health fund, or ensuring you have adequate health insurance coverage that continues post-retirement (including critical illness and top-up plans).

Investing Based on Emotion

Financial markets are inherently volatile. It’s easy to get caught up in market euphoria during bull runs (buying high) or panic during downturns (selling low). Making investment decisions based on fear or greed, rather than a long-term strategy and asset allocation plan, can severely harm your portfolio returns. Stick to your plan, invest systematically (like through SIPs), avoid timing the market, and focus on your long-term goals.

Inadequate Insurance Coverage

Your retirement plan relies on your ability to earn and save consistently over many years. Unforeseen events like premature death, disability, or critical illness can disrupt your income and deplete savings meant for retirement. Having adequate life insurance (term insurance) protects your family’s financial future and your retirement goals if you’re not around. Sufficient health insurance protects your savings from being wiped out by large medical bills. Insurance is the foundation upon which a sound financial plan is built.

For Small Business Owners: Mixing Business & Personal Finances

Small business owners often face unique challenges. Income can be irregular, and there’s a strong temptation to reinvest all profits back into the business or use business funds for personal expenses. This makes disciplined retirement planning in India difficult. It’s crucial to:

- Maintain strictly separate bank accounts and records for business and personal finances. One key step is to Set Up An Accounting System for My Small Business.

- Pay yourself a regular ‘salary’ from the business, even if it’s modest initially.

- Automate personal savings and investments (e.g., SIPs, PPF/NPS contributions) from your personal account as soon as you receive your ‘salary’.

Treating personal retirement savings as a non-negotiable ‘business expense’ is vital for entrepreneurs.

How TaxRobo Can Support Your Journey to Plan for Retirement

Navigating the complexities of financial planning, investments, and taxation can be overwhelming. While this guide provides a framework, personalized advice and execution support can make a significant difference in achieving your retirement goals. This is where TaxRobo can assist you. As experts in Indian finance and legal matters for small business owners and salaried individuals, we understand the nuances involved when you plan for retirement.

We offer several services that align with your retirement planning needs:

- Personalized Tax Planning: Our experts can help you structure your investments tax-efficiently, ensuring you maximize benefits under sections like 80C, 80CCD(1B), etc., thereby enhancing your net returns. We provide personal financial planning tips India focused on tax optimization related to retirement products like NPS, EPF, PPF, and Mutual Funds.

- Financial Structuring for Small Business Owners: We assist entrepreneurs in setting up clear financial distinctions between business and personal finances, facilitating disciplined savings habits essential for long-term goals like retirement. We can guide you on compliance and optimal ways to draw income for personal investment.

- Compliance Guidance: We can help ensure your investment-related activities remain compliant with Indian tax laws and regulations, offering peace of mind.

TaxRobo aims to be your trusted partner in achieving financial security. While we don’t offer direct investment advisory, our expertise in tax and financial structuring provides a critical support layer for your retirement planning journey. Consider reaching out for an Online CA Consultation to discuss how we can help tailor tax strategies to support your retirement savings plan.

Conclusion

Successfully navigating how to plan for retirement in India is fundamentally about taking control of your financial future through disciplined personal financial planning. It’s a journey that begins with defining your retirement vision and meticulously assessing your current financial standing. Calculating your target corpus, factoring in the crucial element of inflation, sets the destination. Crafting a diversified savings and investment strategy, tailored to your risk profile and time horizon, paves the way. Integrating smart tax planning maximizes your returns, while regular monitoring and adjustments ensure you stay on course despite life’s inevitable changes. Remember, the key steps involve goal setting, assessment, calculation, strategic investing, tax planning, and consistent reviews.

The path to a secure and comfortable retirement requires consistent effort and informed decisions. Avoiding common mistakes like delaying the start, underestimating inflation, or making emotional investment choices is just as important as following the right steps. Whether you are salaried or run your own business, the principles remain the same: start early, save regularly, invest wisely, manage taxes efficiently, and stay the course. Your future self will thank you for the commitment you make today to plan for retirement. Don’t delay – start your retirement planning in India journey now. For personalized guidance on tax planning and financial structuring to support your retirement goals, consider seeking professional advice. TaxRobo is ready to assist you with expert insights and services tailored to your needs.

Frequently Asked Questions (FAQs)

- Q1. How much money do I realistically need to plan for retirement comfortably in India?

Answer: There’s no single magic number, as the “comfortable” amount is highly subjective. It depends entirely on your desired retirement lifestyle (modest vs. luxurious), your expected annual expenses (adjusted for inflation), where you plan to live, your chosen retirement age, and your life expectancy. Instead of seeking a generic figure, focus on Step 3 of this guide: calculate your specific target corpus based on your projected expenses and financial situation. - Q2. Are EPF and PPF enough for my retirement plan?

Answer: EPF and PPF are excellent foundational tools for retirement savings in India, offering safety, tax benefits (EEE status), and decent returns for the debt portion of your portfolio. However, they might not be sufficient on their own for several reasons. PPF has an annual contribution limit (currently ₹1.5 Lakhs). EPF contributions are linked to your salary. Depending on your retirement goals and lifestyle aspirations, the corpus generated solely from EPF/PPF might fall short, especially considering inflation. Diversification into other asset classes like equity (through NPS or Mutual Funds) is usually necessary to generate higher long-term growth and build an adequate corpus. - Q3. As a small business owner, how does my approach to retirement planning in India differ?

Answer: While the core principles are the same, small business owners face unique challenges requiring specific approaches. Key differences include:- Income Irregularity: Need greater discipline to save consistently during high-income periods to cover low-income periods.

- Business/Personal Finance Separation: Crucial to maintain separate accounts and treat personal savings as a mandatory ‘expense’.

- Investment Choices: Can fully utilize PPF and NPS (as self-employed individuals get the full tax benefits, including the employer contribution equivalent under certain structures).

- Contingency Planning: Need robust emergency funds and insurance (life, health, business liability) as business risks can impact personal finances directly.

- Effective personal finance management for retirement in India is particularly critical for entrepreneurs to ensure long-term security is not sacrificed for business growth.

- Q4. What are the most tax-efficient retirement savings strategies for Indians?

Answer: Several investment options offer significant tax benefits, making them efficient for retirement planning:- Public Provident Fund (PPF): EEE status (contribution deductible under 80C, interest and maturity tax-free).

- Employee Provident Fund (EPF): EEE status (employee contribution deductible under 80C, employer contribution exempt up to a limit, interest and withdrawal generally tax-free subject to conditions).

- National Pension System (NPS): EET benefits (employee contribution deductible under 80C & exclusive ₹50k under 80CCD(1B), employer contribution deductible under 80CCD(2); 60% lump sum withdrawal at 60 is tax-free, annuity taxable).

- Equity Linked Savings Scheme (ELSS): Mutual funds with 3-year lock-in, contribution deductible under 80C. Returns are taxed as Long-Term Capital Gains (LTCG) at 10% above ₹1 Lakh per year.

- Sovereign Gold Bonds (SGBs): Interest is taxable, but capital gains on redemption at maturity (8 years) are tax-free.

- Remember, tax laws can change, so always verify the current rules.

- Q5. How often should I revisit my retirement fund planning India?

Answer: It’s highly recommended to review your retirement plan thoroughly at least once a year. This allows you to track progress, check investment performance against benchmarks, reassess assumptions (like inflation, return expectations), and make necessary adjustments to your savings or asset allocation. Additionally, you should revisit your plan whenever a major life event occurs, such as:- Significant salary increase or decrease

- Marriage or divorce

- Birth of a child

- Job change (especially impacting EPF/NPS)

- Receiving a large inheritance or windfall

- Major change in financial goals or retirement timeline

- Significant market movements impacting your portfolio value.

Regular reviews keep your plan relevant and aligned with your evolving life circumstances.